The unemployment rate fell to 8.1 percent in August, according to today’s employment report, which is the lowest rate since the onset of the recession. The private sector added more than 100,000 jobs, continuing a steady recovery that has added 4.6 million jobs over the last 30 months. In contrast to previous recoveries, as we discussed in last month's job posting, public sector employment has continued to decline, which has restrained overall job gains.

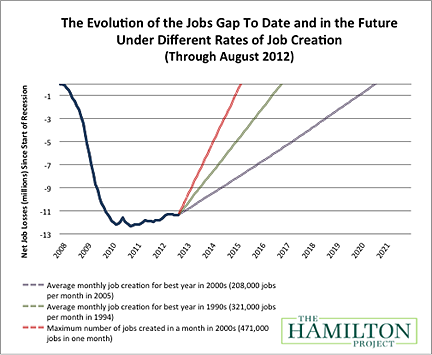

As of August, our nation faces a “jobs gap” of 11.3 million jobs. The chart below shows how the jobs gap has evolved since the start of the Great Recession in December 2007, and how long it will take to close under different assumptions of job growth. The solid line shows the net number of jobs lost since the Great Recession began. The broken lines track how long it will take to close the jobs gap under alternative assumptions about the rate of job creation going forward.

If the economy adds about 208,000 jobs per month, which was the average monthly rate for the best year of job creation in the 2000s, then it will take until August 2020 – or eight years – to close the jobs gap. Given a more optimistic rate of 321,000 jobs per month, which was the average monthly rate of the best year of job creation in the 1990s, the economy will reach pre-recession employment levels by October 2016 – not for another four years.