According to last Friday’s employment report from the Bureau of Labor Statistics (BLS), employers added 169,000 jobs in August, about the same monthly pace of job creation that has prevailed over the past three years. This pattern of modest growth is also reflected in other labor-market indicators, including the unemployment rate, which has steadily edged down from 8.1 percent in August 2012 to 7.3 percent last month. However, the broadest measure of employment—the employment-to-population ratio—was 58.6 percent and has remained close to that level for several years.

Despite the consistent pattern of monthly gains, the nation’s goal of a full economic recovery remains elusive. One factor driving this outcome is an unclear definition of what “recovery” actually means. Indeed, fiscal and monetary policymakers have suggested a wide variety of economic goals. For instance, the Federal Reserve Board has suggested it will reconsider its unusually low interest rate policy when the unemployment rate falls to 6.5 percent. Fiscal policymakers have been even more conservative in their expectations, cutting budget deficits rapidly, and facilitating large cuts to government employment even as unemployment has remained elevated.

These actions appear to reflect policymakers’ dramatically reduced expectations for what constitutes the new normal of economic recovery. The tepid jobs growth of the last five years has discouraged many workers, who have dropped out of the labor force altogether or chosen not to enter the job market in the first place. One measure of these lowered expectations is the difference between the actual size of the American labor force today (i.e., the number of individuals who are employed or are actively seeking a job) and forecasts of the labor force formed near the start of the recession: there are approximately six million fewer workers in the labor force than expected. Why does this matter? Because the unemployment rate only measures the extent to which those looking for work can find a job, setting recovery standards that are tied to the unemployment rate risks ignoring these missing workers.

In this month’s employment analysis, The Hamilton Project explores the “jobs gap,” or the number of jobs the economy would have to add to offset the effects of the Great Recession, which we offer as a useful target for economic recovery. The analysis discusses how changes in population and labor-force participation rates will affect the time it takes to close the gap and how we measure progress toward our economic recovery.

The Six Million Missing Workers

Over the past several years, projections in labor-force growth have been revised sharply downward. These revisions are largely the result of two trends that have emerged in the wake of the Great Recession.

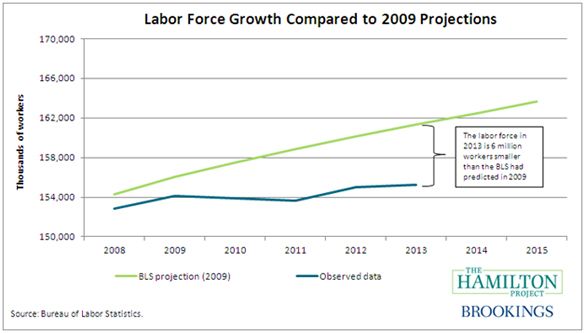

First, the net rate of immigration to the United States slowed significantly as employment opportunities became scarcer. As figure 1 illustrates, there are currently 1.9 million fewer working-age individuals in the United States than the BLS had projected in 2009 (before the Great Recession’s extent was fully evident). This decline in immigration significantly reduced the size of the labor force and hence the number of jobs the economy needs to add each month to keep up with labor-force growth.

Figure 1

Second, the labor-force participation rate—the share of the population that is actively working or seeking work— has declined and is now expected to remain depressed for years to come. Figure 2 illustrates that, even if we ignore the slower-than-expected population growth, there were fewer workers in every age category than the BLS had predicted in 2009. The decline of 2.1 million workers between twenty-five and fifty-four years of age is especially troubling because these are the prime working years. (By comparison, the decline in the labor force among sixteen- to nineteen-year-olds at least partially reflects decisions to remain in school longer, which could be a silver lining of the Great Recession.) Summing across all age categories, the reduction in labor-force participation causes today’s labor force to be 4.7 million workers smaller than the BLS had projected in 2009.

Figure 2

Putting these two effects together, the changes in population and labor-force participation rates mean that the current labor force is much smaller than economists had predicted several years ago. As illustrated in figure 3, there are about six million fewer workers today than the BLS had projected in 2009.

Figure 3

This slow growth of the labor force has important consequences for how policymakers measure progress towards our economic recovery. For instance, consider the Federal Reserve Board’s focus on a 6.5 percent unemployment rate. Taking the current labor-force participation rate (63.2 percent), if the economy continues adding 169,000 jobs each month—as it did in August—the unemployment rate would drop to that level before the end of 2014. But, again, that relatively low labor-force participation rate is largely a consequence of the Great Recession. If we instead take the 2013 projections of the labor-force participation rate that the BLS had forecast in 2009 (65.4 percent), then the same pace of job creation would not bring the unemployment rate down to 6.5 percent until 2021. In other words, if policymakers exclusively use the unemployment rate to guide their decisions, they will not achieve a full recovery from the Great Recession, and instead will be settling for a new normal.

The Jobs Gap as a Recovery Target

In May 2010, The Hamilton Project introduced a summary measure of recovery: the “jobs gap,” or the number of jobs it would take to return to employment rates projected before the onset of the Great Recession. This benchmark, we suggest, is a better recovery target than what has been proposed thus far by policymakers. The jobs gap is calculated under the assumption that employment trends that had prevailed prior to the recession would have continued. Therefore, when labor-force growth is slowed due to a sluggish economy, the jobs gap does not automatically become easier to close, as is the case when policymakers exclusively target the unemployment rate.

Between the onset of the Great Recession in December 2007 and the low point of employment in February 2010, payroll employment in the United States fell by 8.7 million. But these lost jobs are only one of the contributors to the jobs gap. The jobs gap also take into account the influx of new workers into the labor market. Consequently, closing the jobs gap means that the U.S. economy must generate enough jobs to make up for those that were lost as a direct result of the Great Recession and to accommodate these new workers.

Calculating the jobs gap and estimating how long it will take to close that gap, then, requires knowledge of how the labor force is changing. That, in turn, requires projections well into the future of population growth, immigration, and the decisions of individuals about whether or not to actively pursue employment—variables that depend partially on the state of the economy.

The changes in the 2013 population and labor-force participation, relative to 2009 projections, that were described above are largely due to the Great Recession, and this poses a challenge for calculating the jobs gap. The purpose of the jobs gap is to estimate the number of jobs that the economy must add to eliminate the negative consequences of the recession. If the growth of the labor force is slower-than-expected because the recession has discouraged individuals from seeking work, it would not make sense to accordingly lower the number of jobs required each month to keep up with labor-force growth; after all, this low growth rate is itself a negative consequence of the recession. On the other hand, it is appropriate to reduce the jobs gap for lower-than-expected population growth.

The August Jobs Gap

Beginning this month, we base the jobs gap calculations on labor-force forecasts from the Congressional Budget Office (CBO), rather than from pre-recovery projections from the Bureau of Labor Statistics as we have done previously. The CBO forecasts provide a more consistent series of estimates, are updated and revised more regularly, and reflect CBO’s estimates of growth in the potential level of economic output. As a result, we feel they are better suited for capturing the intent of the jobs gap. This is discussed in more detail in the technical appendix.

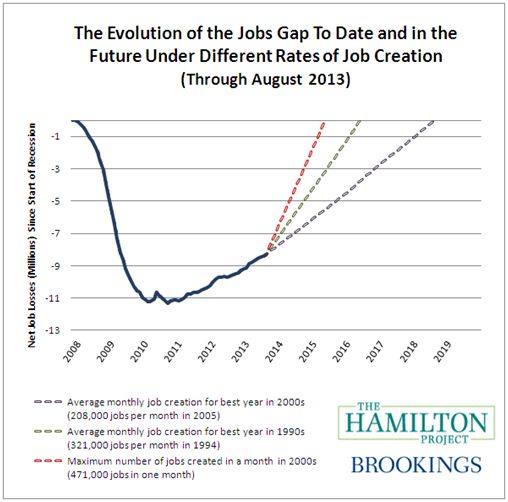

As of the end of August, our nation faces a jobs gap of 8.3 million jobs (compared to 9.7 million with our previous methodology). Figure 4 below shows how the jobs gap has evolved since the start of the Great Recession in December 2007, and how long it will take to close under different assumptions of job growth. The solid line shows how the jobs gap has evolved since the Great Recession began. The broken lines track how long it will take to close the jobs gap under alternative assumptions about the rate of job creation going forward.

Figure 4

If the economy adds about 208,000 jobs per month, which was the average monthly rate for the best year of job creation in the 2000s, then it will take until August 2018 to close the jobs gap. Given a more optimistic rate of 321,000 jobs per month, which was the average monthly rate of the best year of job creation in the 1990s, the economy will reach pre-recession employment levels by June 2016.

To explore the outcomes under various job creation scenarios, you can try out our (updated) interactive jobs gap calculator by clicking here. You can also view the jobs gap chart for each state here.

Conclusion

More than four years after the official end of the Great Recession, many American workers are still feeling the effects from the worst economic downturn since the Great Depression. Indeed, the current labor force has about six million fewer workers than had been projected in 2009, largely due to the Great Recession. It is tempting to settle for a new normal, but the economy will not be fully recovered until today’s missing workers are back at work.