To provide an economic context for tax reform, The Hamilton Project has a set of economic facts focusing on the role of our tax system in the long-run budget deficit, global competitiveness, and rising income inequality.

Introduction

Taxes and tax policy are on the table for discussion. Policymakers continue to look at tax cuts— most recently, the payroll tax cut and reductions for small business—as instruments for aiding the nation’s economic recovery. And, fiscal issues will continue to dominate the policy agenda as the federal government faces the expiration of the Bush-era tax cuts, the onset of the deficit “trigger,” and another debate over the debt limit—all colliding at the end of 2012. Across the political spectrum, one of the few points on which today’s policymakers agree is that the tax code is in desperate need of reform in order to be able to contend with issues ranging from American competitiveness to income inequality.

To further complicate these challenges, today’s tax reform debates are often based on misconceptions or lack good evidence. To that end, The Hamilton Project aims to provide a series of facts that can help ground the policy discussion. They are presented in the spirit of the late U.S. Senator Daniel Patrick Moynihan’s famous saying, “Everyone is entitled to his own opinions, but not to his own facts.”

Read the full introduction

Since the last major tax reform in 1986—roughly a generation ago—the number of loopholes, special preferences, and the sheer volume of the tax code have ballooned, resulting in a system widely considered to be inefficient, complex, and unfair, as well as an impediment to growth. Drawing a page from successful prior reform efforts, advocates of comprehensive tax reform generally urge that we broaden the base and lower rates.

However, the current economic context for tax reform is far more challenging than it was in 1986. Most immediately, the economy is still in the midst of a slow recovery with an unemployment rate that remains too high. Even with robust rates of job growth, it will take years to close the jobs gap. An important role of fiscal policy in the near term is to support recovery in the labor market.

But in the longer run, the United States is contending with three economic problems: a daunting outlook for budget deficits that imperils our well-being, an increasingly competitive global economy for many American workers and industries, and rising income inequality. The tax code interacts with each of these problems, and a successful tax reform effort will need to address each of them—or at least avoid making any of them worse.

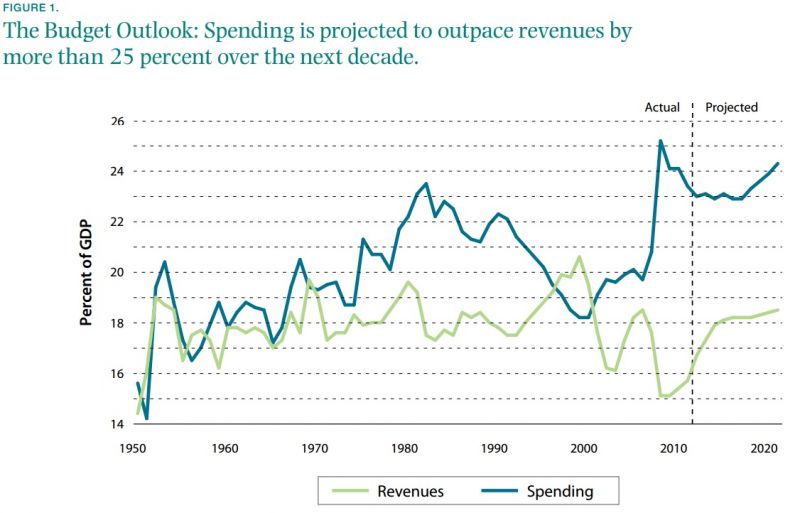

Long-Run Budget Deficit. First, the gap between what the government spends and what it receives in tax revenues is expected to widen even after the economy recovers from the effects of the Great Recession, contributing to a spiraling debt (Figure 1). While it is natural—indeed economically beneficial— to run a deficit today to support the nascent recovery, left unchecked the deficit will remain above $1 trillion in 2020 and the national debt will rise to 89 percent of GDP and continue rising, imposing significant hardship on future generations of Americans and impairing our economy’s ability to grow.

Addressing the long-run deficit will require a hard look at both spending programs and tax revenues. While revenues are currently low due to economic conditions and the need to support near-term growth, current tax policies will not produce enough revenue to cover spending—even after the economic recovery—for Social Security, Medicare and Medicaid, defense, and interest on our debt, let alone any other government services. In fact, the average level of annual tax revenues projected over the next decade would not have resulted in a balanced budget in any of the past forty years. Put another way, we will collect less in revenues in future years than we have spent in each year of the past four decades—and this comparison understates the challenge, as an aging population and the continuing rise in healthcare costs will increase federal spending above historical levels. Even setting aside new expenditures that policymakers could reasonably consider, we are facing a hard truth: in order to rein in our spiraling budget deficit, sensitive and difficult decisions must be made regarding higher tax revenues and cuts to even the most sacrosanct social security, health, and national defense programs.

Increasingly Competitive Global Economy

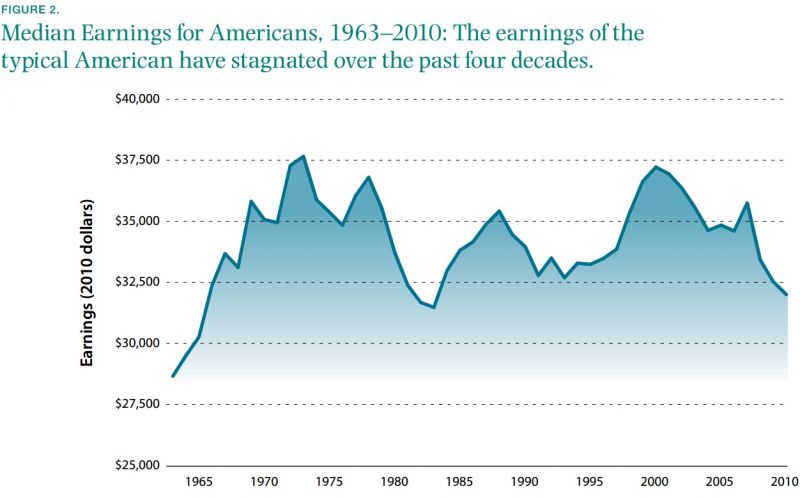

Growing unease about the global competitiveness of American workers and industries presents a second challenge for policymakers. Increasing international competition for business activity, the rise of workforces around the world that are more educated and capable, a slowdown in the pace of U.S. innovation, and low rates of saving and investment by American households have contributed to reduced economic opportunities for many Americans. One sign of these long-run challenges is that the earnings for the typical American have been stagnant for four decades (Figure 2) while the earnings of the typical high-school graduate have actually declined by 14 percent.

Concerns about competitiveness have encouraged greater scrutiny of how our rules and regulations encourage or impede economic activity. Since taxes touch on so many areas of our economy—savings and investment, financial flows, research and innovation, the location of business activity and production, and the government budget—tax reform has been widely touted as having a significant impact on economic growth.

Many proponents of tax reform assert that certain provisions of the tax code stifle economic growth, such as high statutory rates, preferences that subsidize certain activities and investments while penalizing others, and the direct costs related to the complexity of the system and to complying with it. However, these costly and complicated provisions often exist to serve real purposes and important constituencies. For instance, the largest business tax breaks—like incentives for new investment or deductions for domestic production—encourage domestic business activities, while the largest individual tax breaks subsidize health insurance, retirement savings, and home ownership. Adjudicating between these competing demands in order to meet new economic and social challenges will require difficult economic and political trade-offs.

Rising Income Inequality

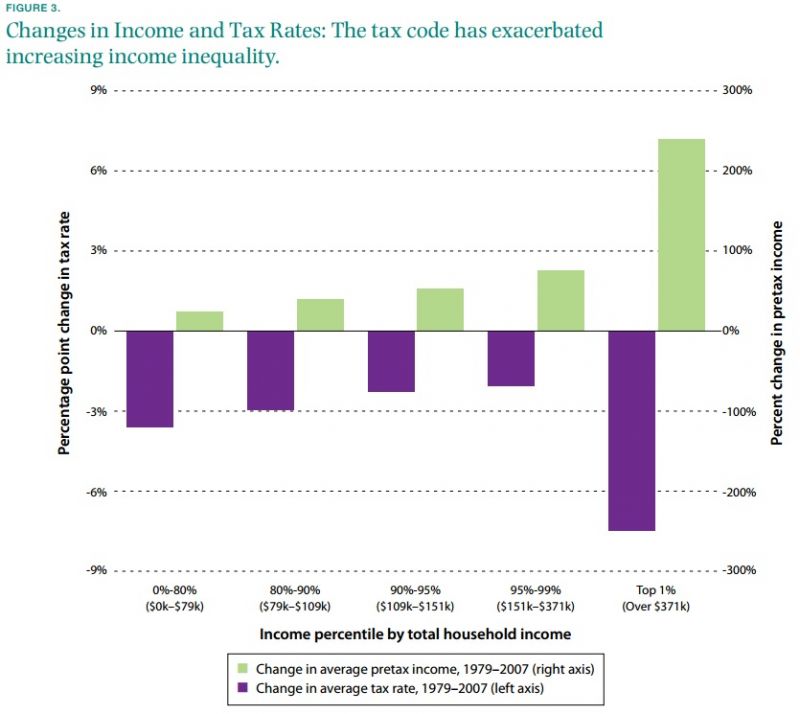

Finally, there is the real and abiding issue of income inequality and its relationship to the tax code. Technological changes, combined with the forces of globalization, have selectively helped some workers over others and have benefited senior managers and owners of capital and businesses more than others. Earnings have risen dramatically at the top since 1979—by more than 250 percent for households in the top 1 percent of the income distribution. At the same time, many households at the middle and bottom have experienced stagnating incomes or even declines in earnings (Figure 3). Widening income inequality for workers has had significant consequences for American families, including greater disparities in the economic situations of children— creating an uneven playing field for future generations.

Changes in the tax system over the past thirty years have exacerbated these problems. The very people who have received the biggest income gains in the past three decades have also seen the largest tax cuts. A progressive tax code that takes ability to pay into account—in which the tax rate increases as taxable income increases—is the most significant and powerful tool available to counteract income inequity. Indeed, given our fiscal challenges, there are increasing calls for policymakers to use the tax code for that purpose.

Unlike prior reform efforts, current tax reform measures must work to update and trim the tax code, while also tackling the twenty-first-century challenges of severe budget deficits, declining international competitiveness for many workers and industries, and growing inequality.

Together, the following facts point to the significant impact our tax system has on America’s economic well-being, primarily by determining how the tax burden will be distributed across households of differing means, and how rising federal indebtedness will affect our future economic conditions. Although tax rates certainly affect economic activity, the best evidence suggests that in most cases these impacts are modest. A successful tax reform effort could play an important role in combating income inequality, and, whencombined with spending cuts, in addressing the nation’s long-run budget deficit.

This paper is in two parts:

Part 1. The first half of the paper presents five key facts about the tax system as it relates to the budget, American competitiveness, and inequality.

Part 2. The second half of the paper illustrates various criteria for evaluating tax reform options, based on practical tradeoffs between revenues, rates, and progressivity, and in terms of how alternative options affect the budget, American competitiveness, and inequality.

Part 1: The Economic Context of Tax Reform

Fact 1: America collects lower revenues than other industrialized countries.

The basic purpose of the tax system is to raise revenues to pay for government services. In this regard, the U.S. tax system comes up short: in 2015, the federal government is projected to spend about $12,400 per American but receive only $9,700 per person in taxes. Closing this gap will require overhauling government finances, and likely mandating changes in both revenues and spending.

What is the right level of tax revenues? The answer requires making choices regarding the size of government spending and how the tax system should influence the distribution of economic well-being. One commonly used benchmark is historical and projected spending. According to the Congressional Budget Office (CBO), federal spending has averaged 21 percent of GDP over the past thirty years and is projected to be 23 percent of GDP over the next ten years (CBO 2012b). (Over the same historical period, revenues averaged only 18 percent of GDP.) However, the historical spending benchmark is misleading because increases in government spending are increasingly the product of two irreversible forces: the aging of the population and the rise in healthcare spending. Because of these factors, spending for Social Security, Medicare, and Medicaid—programs that will compose 64 percent of the federal budget in 2020—are unlikely to return to their lower historical levels. Thus, prior levels of revenues will no longer suffice to hold down deficits in the face of these future challenges.

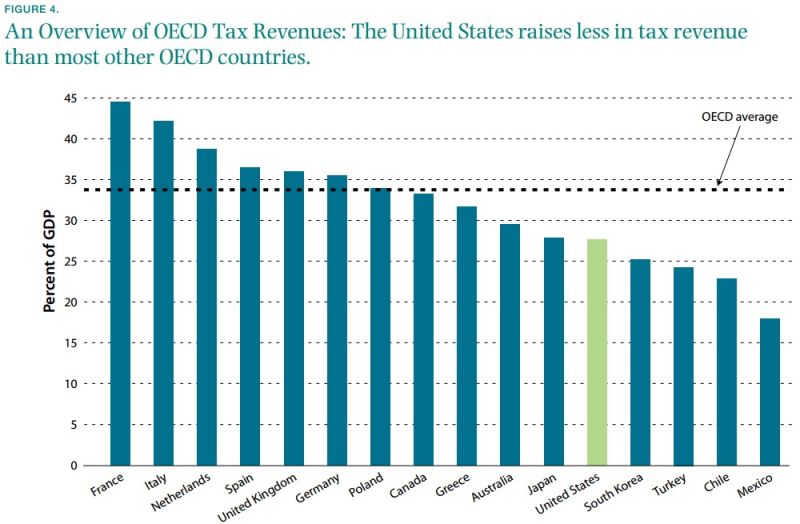

A second benchmark examines tax rates imposed by comparable developed economies. In comparison to many of its competitors, the level of U.S. government spending is below average. The level of U.S. revenue collection, however, is near the bottom. Figure 4 compares total taxes raised in various countries, including federal, state, and local taxes, and valueadded taxes (VATs). In the three years (2005–2007) before the recent recession, Germany raised an average of 36 percent of its GDP in taxes, while the United States raised just 28 percent, above only South Korea, Turkey, Chile, and Mexico. On average, other OECD countries raised 34 percent of GDP in taxes each year. To put the magnitude of these differences in perspective, if the United States were to raise tax revenues to the OECD average, approximately 6 percent of GDP higher than our current level, and maintained currently scheduled spending, the entire national debt could be paid off in roughly nineteen years.

In addition to its outlier status among developed economies in terms of its level of tax revenues, the United States is also different in terms of how it raises those revenues. The United States is the only OECD country that does not have a VAT—a form of consumption tax—as part of its system, making it particularly reliant on income and payroll taxes. In fact, an average of 30 percent of all tax revenue in non-U.S. OECD countries came from consumption taxes in the three years prior to the recent recession, compared to only 18 percent of revenue in the United States. Economists generally favor taxes on consumption over taxes on income because of the reduced tax burden imposed on new investments, which are an important driver of economic growth.

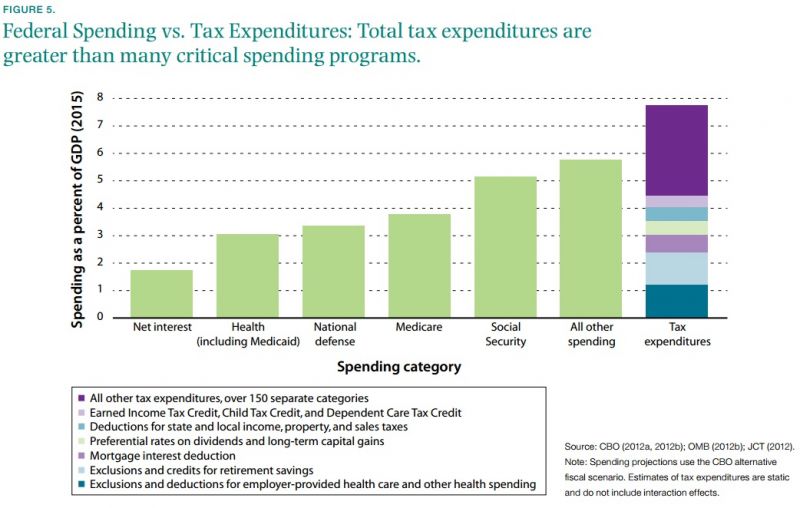

Fact 2: Tax expenditures represent a large share of total government spending.

One of the primary reasons America’s tax revenues remain low relative to other industrialized countries is our use of special tax preferences, or “tax expenditures,” that provide individuals and businesses with opportunities to reduce their tax bills by undertaking certain actions.

The fact that these expenditures operate through the tax code helps mask the fact that, in dollar terms, these tax preferences are very large. As Figure 5 shows, the magnitude of tax expenditures is comparable to the largest government spending programs; in total, they are about 8 percent of GDP.

These preferences can interfere with the normal operation of market forces by artificially encouraging some economic activities over others, sometimes with undesirable effects. For example, the tax code offers a break for taxpayers who deduct mortgage interest. A direct result is that the government forgoes tax revenue that it would otherwise have collected. An indirect result is that some Americans choose to buy larger homes and to borrow more to finance them, resulting in higher indebtedness instead of more-profitable or less-risky investments elsewhere.

The mortgage interest deduction and similar tax breaks are referred to as “tax expenditures” because they add to the deficit to subsidize certain activities, just as some spending programs do. Eliminating or limiting tax expenditures could raise revenues to reduce the federal deficit or to facilitate lower tax rates. However, reining in tax expenditures will not be easy. First, many tax expenditures serve important purposes, such as offsetting the tax burden on working families or promoting health insurance coverage. Additionally, the largest tax expenditures—such as the tax breaks for mortgage interest, health care, and retirement savings, and reduced rates for capital gains—are also the most entrenched tax expenditures, and are defended by a broad base of vocal stakeholders.

Fact 3: The tax code subsidizes some activities and penalizes others.

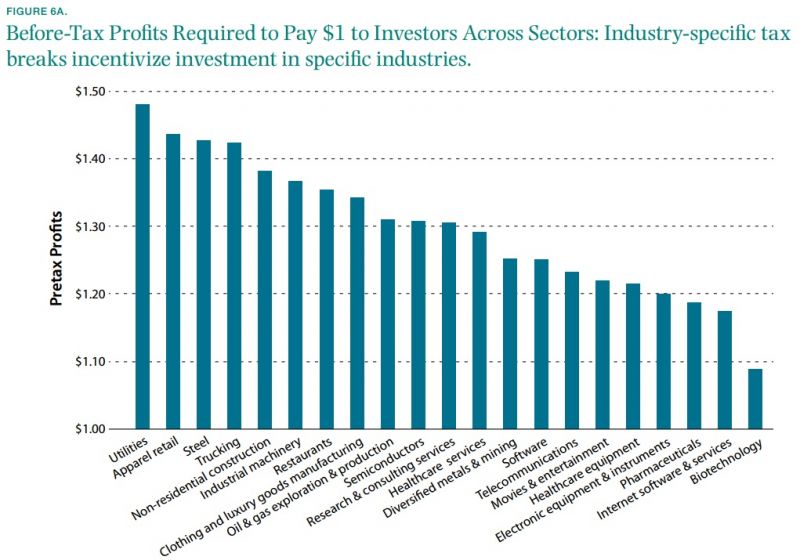

The tax code assigns different tax rates to different activities by incentivizing some activities while penalizing others. When it treats economic activities differently, it makes certain activities more or less profitable. There is little doubt that these differences guide investment decisions and ultimately the form of the U.S. economy—e.g., the industries that are located in the United States and the types of jobs available to American workers. While some of these differences arise for specific purposes such as the credit for research and experimentation that may have broader benefits, many differences arise unintentionally, when, for example, historical rules fail to adapt to changing economic circumstances. The result is that our economy fails to pursue the activities with the greatest economic benefits for businesses and their workers. The system of differential effective rates of taxation amounts to an industrial policy that picks “winners” and “losers,” without necessarily favoring industries that are likely to generate benefits to the broader economy.

For example, the corporate tax system’s effective marginal corporate tax rate was about 23 percent in 2007, but this is only an average as it assigns widely different effective rates to different activities and industries. Figure 6A shows how these different effective rates translate into pretax profitability. Companies in high-tax industries, such as steel, trucking, or utilities, must earn more than $1.40 in before-tax profits, on average, to return $1 to investors. On the other hand, companies in low-tax industries, such as biotechnology and Internet services and software, need to earn less than $1.20.

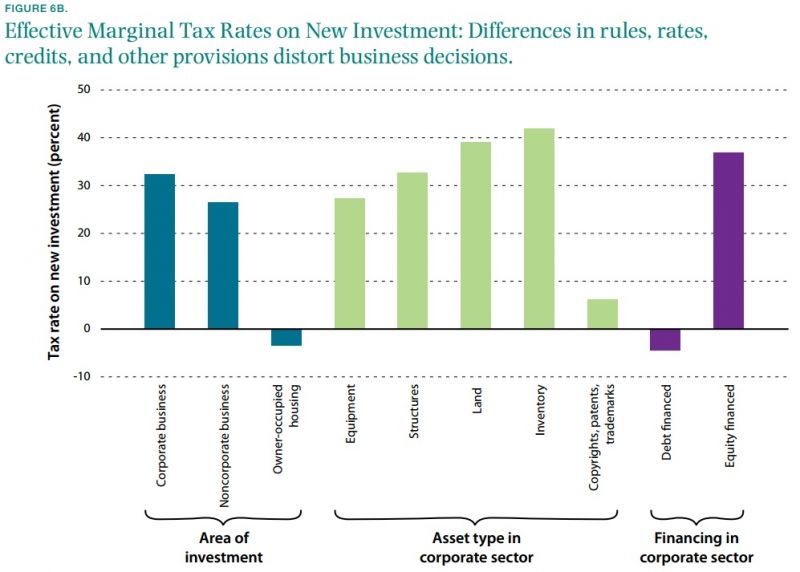

Furthermore, these features of the tax code also affect the types of investments that businesses make, beyond just which industry to invest in. Figure 6B illustrates that various rules, rates, credits, and other provisions in the business tax system cause very different tax rates for different activities and economic choices. For instance, within every industry the tax system favors investment in certain kinds of equipment and assets over others. The tax system also rewards certain types of financing, since corporations are able to deduct interest paid, but not dividends paid, from their taxable income. This preference encourages businesses to raise funds by taking out debt rather than by issuing stock—resulting in higher risks of business bankruptcy.

Similarly, other provisions in the tax system favor noncorporate businesses over those that are in the corporate sector. Corporate income is subject to tax at two levels—once when it is earned by the corporation and again when it is paid to shareholders as dividends or when shareholders sell appreciated stock. But noncorporate business income from partnerships, sole proprietorships, and other noncorporate businesses is not subject to the corporate tax, despite the fact that many of these organizations share many characteristics of corporations. Instead, income from a “pass-through” business passes through to the individual income tax returns of the business’s shareholders and owners and is taxed only on its owners’ individual returns. This creates an economic distortion favoring noncorporate businesses over corporate businesses.

Finally, it is important to note that tax rates on investments in productive businesses are much higher than tax rates on alternative investment options. Investment in owner-occupied housing, for example, is taxed at a rate of –3.5 percent, compared to investment in structures or land by corporate businesses, which are taxed at more than 30 percent.

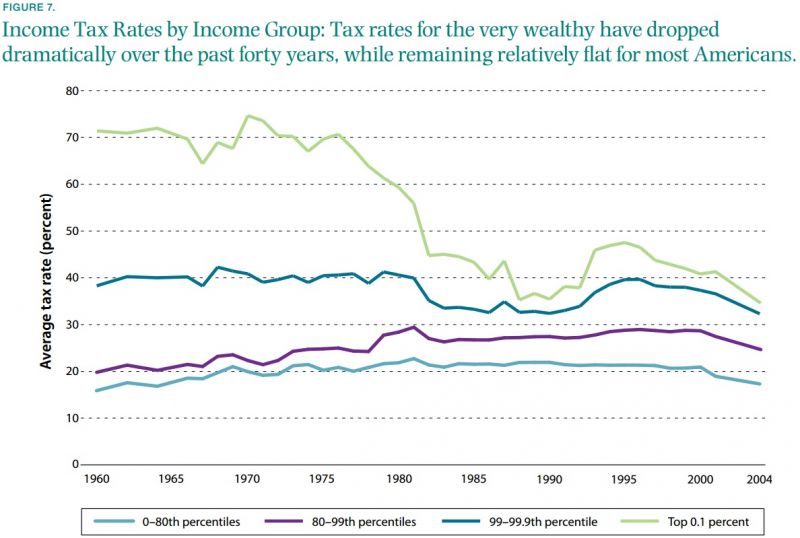

Fact 4: The tax system has become less progress over time.

Over the past four decades, changes in technology, increases in international competition, and other changes in the labor market, such as the decline of unions and a falling real minimum wage, have reduced job opportunities and wages for some American workers but expanded opportunities and incomes for others. While incomes have stagnated and even declined for some at the middle and bottom, incomes at the top have risen dramatically.

As inequality has increased and the divide between the haves and the have-nots has widened, changes in tax policy have exacerbated the market trends, promoting greater inequality among American families. Indeed, tax rates for the wealthiest Americans have declined over the past several decades, while tax rates for average Americans have remained roughly constant. In 1960, the top 1 percent of Americans earned about 10 percent of all income in the United States and paid 22 percent of all federal taxes. While the share of income earned by the top 1 percent had almost doubled by 2004—to nearly 20 percent of all income—the share of tax liability paid by that group had increased by only 24 percent to 28 percent. In short, the federal tax system is becoming less progressive (Figure 7).

In addition to federal taxes, families face state and local tax systems that are, on net, regressive. For instance, families in the bottom 20 percent of the income distribution face state and local tax rates of 12 percent compared to only 8 percent among the top 1 percent of families (CTJ 2012). All told, the total U.S. tax system—including federal, state, and local taxes—is considerably less progressive than the federal tax system.

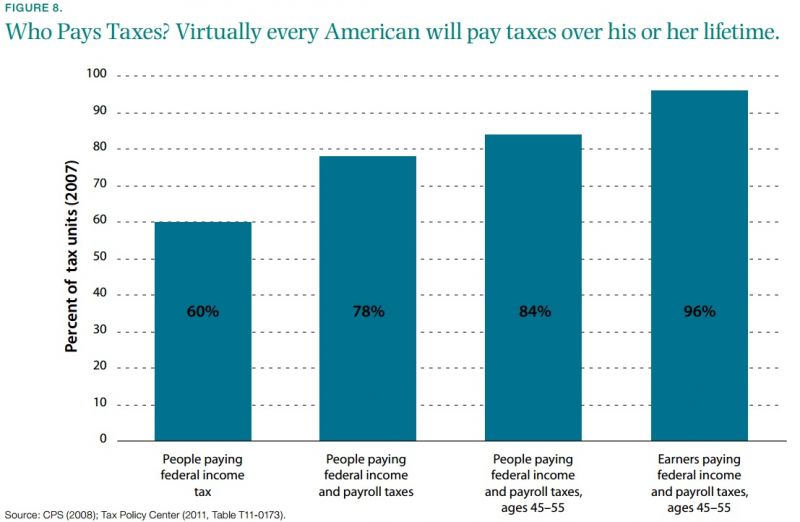

Fact 5: Virtually all American families, even low-income families, pay taxes.

Tax credits for low-income working families, like the Earned Income Tax Credit (EITC) the Child Tax Credit (CTC), and the Dependent Care Tax Credit (DCTC) have helped reduce poverty, provide economic security, and offset declining labormarket opportunities for low-income workers. These credits reduce or eliminate income tax liabilities and sometimes result in a net income tax refund for low-income families. The expansion of these credits is also one reason why a larger share of U.S. households owes no federal income taxes now than was true in the past. But this story is misleading, because it ignores the most significant tax burdens on workers—the payroll tax and state and local taxes.

While a larger number of families do not pay federal income taxes, it is not true that these households do not pay any form of taxes, as many suggest. In fact, most Americans pay more in payroll taxes than in income taxes. After incorporating payroll taxes, 78 percent of American households paid federal taxes in 2007. But even that statistic is misleading. Those who pay no federal taxes—on payroll or income—are disproportionately young (such as students who will pay taxes after they join the workforce) or old (such as retirees who paid taxes over their lifetimes), or temporarily out of work. When looking at middle-age workers, 84 percent face a net payroll and income tax bill; among those who have a job, the number is more than 96 percent. Even households that receive the refundable EITC will face, on net, a positive tax bill over their lifetimes (Dowd and Horowitz 2008). Furthermore, all consumers bear the burden of state and local property, sales, and income taxes, and excise taxes on items like gasoline, alcohol, and cigarettes. These state and local and excise taxes tend to be regressive, imposing more of a burden on low-income families than on high-income families—the state and local tax burden is roughly twice times as large as the federal tax burden for the bottom fifth of households (CTJ 2012).

In short, virtually every American will pay taxes over his or her lifetime (Figure 8).

Part 2: A Framework for Evaluating Reform

Fact 6: There is a limit to what tax reform can accomplish.

Broadening the tax base can only accomplish so much in terms of lowering rates. Where are the limits?

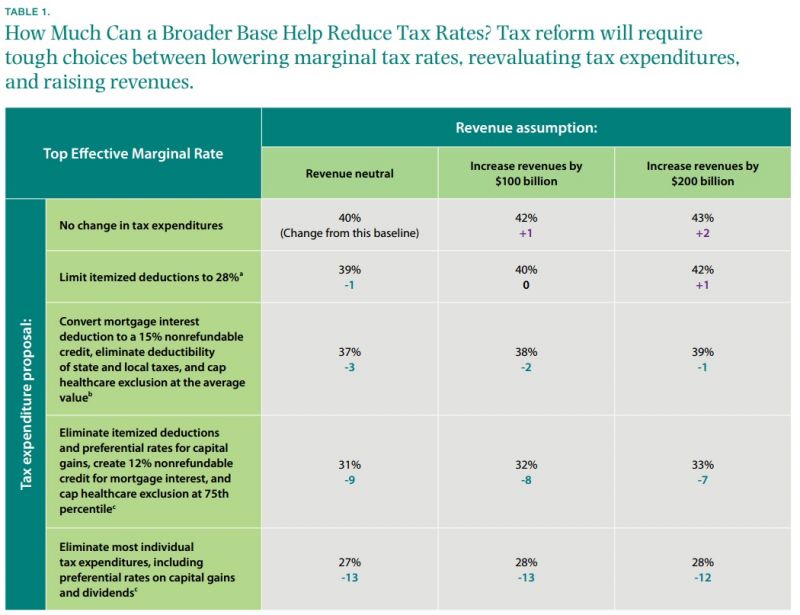

The answer lies in the underlying relationships between rates, tax expenditures, progressivity, and revenues governed by economic constraints. To illustrate these relationships—and the constraints they imply for tax reform—Table 1 examines how tax reforms based on three recent proposals could be used to lower tax rates or raise tax revenues. For each reform, the table estimates the lowest-possible tax rates that raise the specified level of tax revenue while holding constant the distribution of the tax burden within income groups. In other words, how low can rates go before tax revenues fall or the tax system becomes less progressive?

The reforms hold progressivity constant, meaning that average tax payments within income group are held constant in the revenue-neutral case (within groups, however, some individuals face higher or lower taxes), while in revenueraising reforms the after-tax incomes of all groups are reduced by the same proportion.

Income tax rates are scheduled to rise under current law for most taxpayers—up to a level of 40 percent for the top income tax bracket. If policymakers wanted to raise an additional $100 billion in revenues per year by raising tax rates (as opposed to eliminating tax expenditures) proportionately across all taxpayers, then marginal rates on high-income taxpayers would need to rise to roughly 42 percent. Similarly, tax rates on joint filers with about $50,000 in taxable income would rise by about 1 percentage point.

Eliminating tax breaks and broadening the tax base allow for lower tax rates. The second row in Table 1 shows that a modest increase in the tax base—similar to the Obama administration’s proposal to limit the value of itemized deductions to 28 percent—would allow for a modest reduction of 1 percentage point in the top tax rate, while allowing for practically no reduction in lower- and middle-income brackets. A more aggressive approach to base broadening—modeled on the 2005 President’s Advisory Panel on Federal Tax Reform—scaling back the tax benefit of itemized deductions and employer-provided health insurance, would facilitate a reduction of 3 percentage points in rates relative to current law. A more extensive reform—such as the illustrative plan contemplated by the National Commission on Fiscal Responsibility Reform, also known as “SimpsonBowles,” which would eliminate the income tax benefit of all itemized deductions and the preferential rate on capital gains while limiting the benefit of the mortgage interest deduction and the healthcare exclusion—would facilitate a larger reduction in rates of 9 percentage points. Finally, an extremely aggressive reform—such as the “Simpson-Bowles” zero plan, which eliminates most individual tax expenditures, including all those mentioned above—would allow a reduction in rates of 13 percentage points.

These changes are static and do not include potential behavioral responses to lower rates, a topic to which we return later. Moreover, these possible reforms preserve the progressivity of the tax schedule within broad income categories but not amongst families in the same income category, even if they differ in other ways, such as number of children. For instance, many of these proposals imply sometimes sizable shifts in taxes for those who benefit from breaks and those who do not, even if they earn the same income. Preserving progressivity between more narrowly defined groups would place major constraints on base broadening, making efforts to reduce marginal tax rates even more difficult.

Fact 7: Individuals and the economy will feel every approach to tax reform.

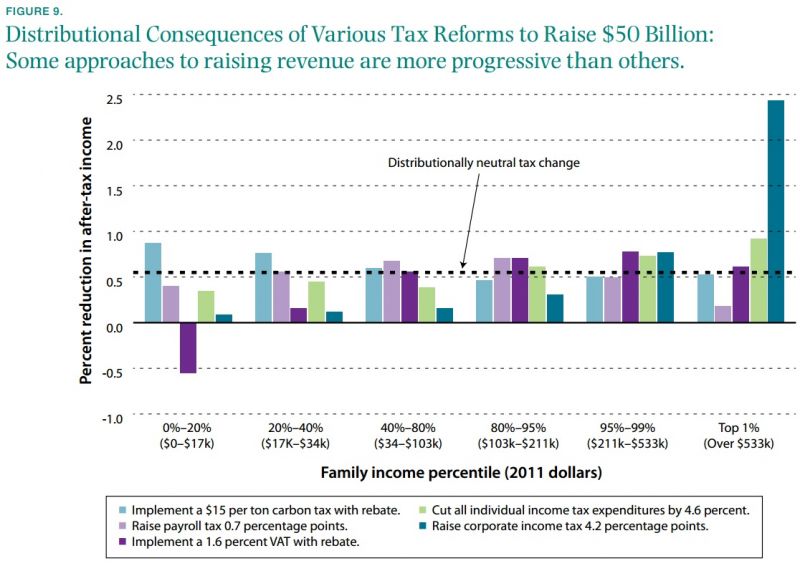

Increasing concern about inequality means that tax changes will be scrutinized on the basis of how they affect the distribution of the tax burden.

Proposals to raise taxes can take many different shapes, from increasing tax rates that are already in the tax code, to implementing new taxes, such as a VAT. Each of these types of taxes will have different effects on the federal budget, individuals, and the economy. Due to rising income inequality, one of the most important aspects of today’s tax reform proposals will be the ways in which they affect taxpayers at different income levels.

In Figure 9, we explore how six proposals to raise $50 billion annually in tax revenues would affect American workers at different segments of the income distribution. As one example, a 1.6 percent VAT with a rebate designed to offset the impact on lowincome families would lower average tax rates among those earning less than $17,000 per year (the rebate is larger than the increased tax burden), have small impacts on those making between $17,000 and $34,000 per year, and reduce after-tax income for higherincome taxpayers by more than 0.5 percent. The chart also shows that corporate taxes—and increases in corporate taxes—are highly progressive, at least under the common assumption that the short-run burden of corporate tax changes falls on owners of corporate businesses. The long-term effects of a corporate tax increase are less certain, as changes in investment decisions over time can affect wages and consumer prices, and therefore spread the burden of the tax to workers and consumers.

Fact 8: The benefits from tax expenditures are not equally shared.

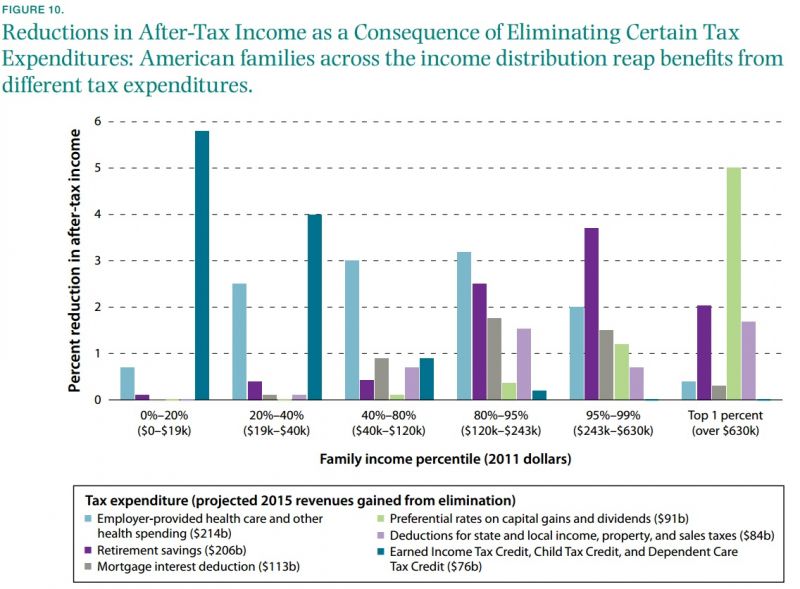

Eliminating or limiting tax expenditures are commonly endorsed tax reform options. The U.S. tax code contains a wide variety of tax expenditures, each of which benefits some groups more than others. For example, the exclusions for employer-sponsored health insurance and the CTC have very different beneficiaries. These exclusions, preferential tax rates, deductions, and credits reduce the tax burden for Americans by allowing them to pay taxes on less of their income or by rewarding them with a lower tax bill for certain behaviors. These tax expenditures also represent lost revenue for the government and can distort individual choices by privileging certain types of spending (such as spending on health insurance through an employer) over other spending.

For these reasons, tax reform proposals often suggest that eliminating tax expenditures can provide revenue for the government. However, as with other approaches to raising taxes, the distributional consequences of reducing tax expenditures depend largely on which tax expenditures are eliminated. Figure 10 presents the distributional consequences of eliminating each of the six largest individual tax expenditures. For instance, family-related tax credits like the EITC, CTC, and DCTC are important for promoting the progressivity of the tax schedule because they primarily reduce taxes paid among low-income working families with children. The reduced rates on capital gains and dividends, which are intended to promote saving, primarily benefit taxpayers in the highest income groups.

Fact 9: Cutting individual income tax rates would modestly increase the earnings of the typical American family while substantially increasing the federal budget deficit.

A key concern among would-be tax reformers is that high tax rates are holding back the U.S. economy and that lower tax rates would not only spur more economic activity, but also help pay for themselves. Fortunately, the question of how individual tax rates influence economic activity is among the most richly studied in the economics of taxation. The simple answer is that individual taxes do affect economic decisions such as how much to work, but only to a modest extent, and that the primary effect of tax cuts is to reduce revenues.

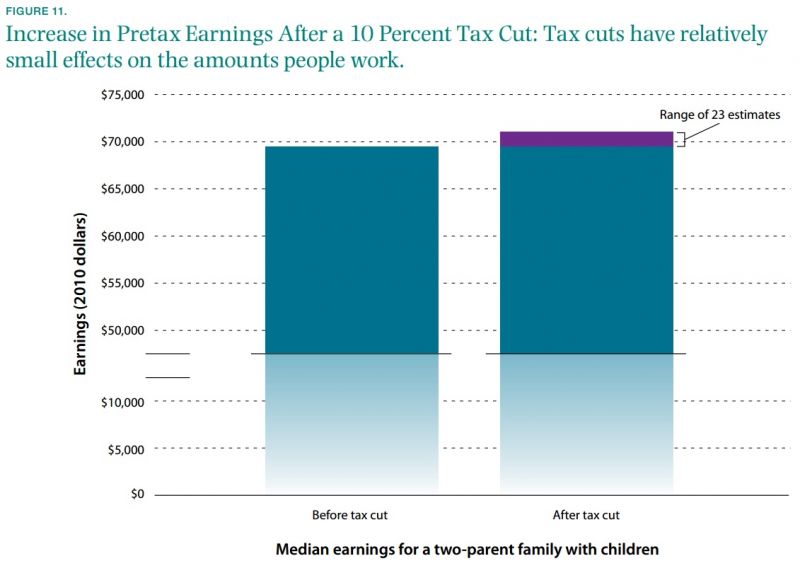

Figure 11 uses the economic evidence from twenty-three published studies cited in Chetty (2011) to illustrate how a 10 percent cut in individual income tax rates might increase the pretax earnings of the typical tax-paying family earning about $70,000 per year. Most studies find that such a tax cut would have essentially no effect on employment or earnings. The average estimate of all twenty-three studies predicts that the typical family would increase pretax earnings by roughly $450, or 0.7 percent. Even using the highest estimated response, the increase in earnings is about $1,500, or about 2.2 percent.

While the household described above would work slightly more, the same evidence also implies that it would pay much less in taxes. Using the fifteen studies that focus specifically on how taxable income (income after subtracting items like mortgage interest or dependent exemptions) responds to changes in tax rates, the same 10 percent tax cut is predicted to reduce federal income taxes paid by 8.6 percent. Far from paying for itself, this tax cut would add to the deficit.

Fact 10: Deficit-financed tax cuts do not spur economic growth in the long run.

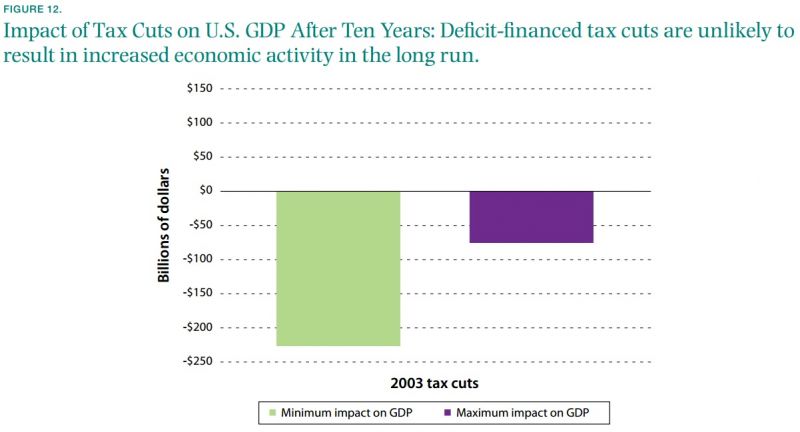

The evidence described in Fact 9 suggests that individual income tax cuts have only modest effects on employment and earnings. But historical tax cuts are also frequently said to have been motivated by a desire to spur economic activity by encouraging increased savings, investment, entrepreneurship, and other activities that contribute to long-term growth. While the evidence suggests that temporary tax cuts can help combat recessions—temporary tax cuts were an important part of the policy response to the Great Recession—the available estimates of how taxes affect the larger economy suggest that in normal economic times any potential long-run gains from lower tax rates are largely offset if they increase the deficit. Instead of increasing saving and investment, tax cuts that result in higher government borrowing reduce funds available to invest in the private sector, reducing growth.

Indeed, the best available estimates suggest that the tax cuts enacted a decade ago likely reduced economic growth in subsequent years. For instance, the CBO estimated the macroeconomic effects of the 2001 and 2003 tax cuts, which reduced revenues by more than $200 billion per year (CBPP 2011).

Although these cuts included many provisions to promote saving, investment, and increased incomes, they also included sizable tax breaks for economic activity that would have happened regardless of changes in tax rates. CBO estimates suggest that the increase in government borrowing to finance the cuts exceeded the benefits of lower tax rates. According to these estimates, illustrated in Figure 12, GDP was reduced by between $75 billion and $226 billion dollars after ten years (CBO 2005).

Fact 11: Corporate tax reform can improve U.S. competitiveness in several different ways—but not necessarily all at once.

When businesses headquarter, invest, and produce their goods and services in America, they help increase U.S. living standards through the jobs they create and the tax revenues they produce. In seeking to promote the United States as a hub for business activity and investment, many have focused on the notion of competitiveness—the idea that policies can attract profitable activities to this country or develop such activities domestically.

For instance, consider calls for the reduction in the U.S. statutory federal corporate rate from its current level of 35 percent in the name of competitiveness. As a standalone policy, a lower corporate rate would enhance incentives for investment, reduce the gap between effective tax rates on corporate businesses and noncorporate businesses, narrow the tax preference for debt financing relative to equity financing, and reduce pressures on multinational firms regarding the location of headquarters, production, or tax avoidance. However, an obvious disadvantage is that each percentage point reduction in the corporate rate reduces revenues by roughly $12 billion per year, leading many to consider revenue-neutral options for corporate tax reform.

By definition, revenue-neutral reform options involve a trade-off between reductions in the statutory rate and an increase in taxes somewhere else. Adjudicating those trade-offs is particularly difficult within the corporate tax system because many of the tax provisions being eyed as revenue raisers are themselves policies intended to promote one specific avenue of competitiveness and often also apply to non-corporate businesses.

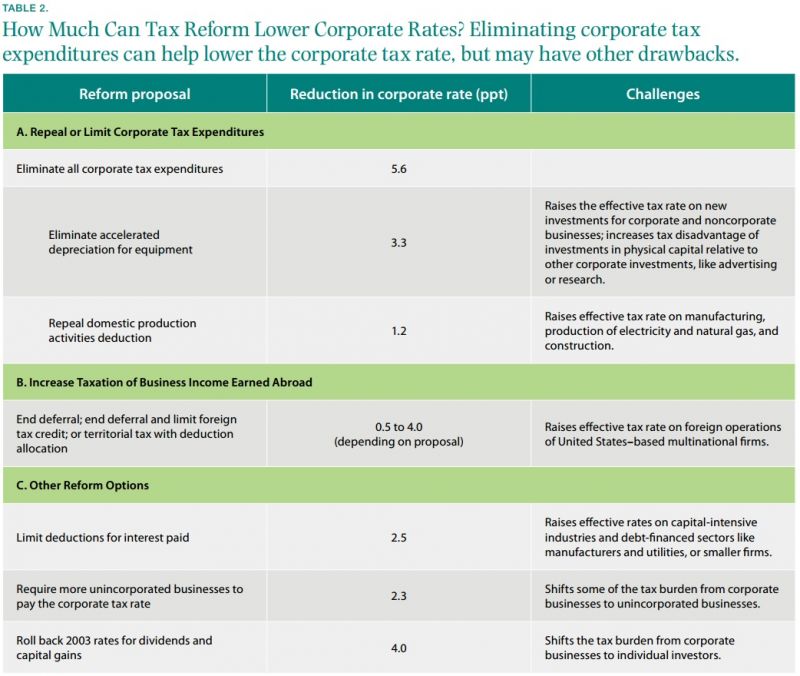

Table 2 illustrates the trade-offs involved in some commonly discussed options for revenue-neutral reforms (CRS 2011). Each option provides for meaningful reductions in the corporate rate. Many would also reduce some of the negative tax distortions discussed in Fact 3 that contribute to inefficiencies in the corporate sector. For instance, limiting the deductibility of interest expense would help equalize the treatment of debt-financed investments relative to equity-financed investments, and reviewing the boundary between corporate and noncorporate businesses could help level the playing field between similar businesses currently operating under unequal tax regimes.

But even seemingly beneficial reforms are not without potential economic or political drawbacks. For each proposal, Table 2 highlights one or more key concerns for implementation, which range from reducing incentives for new investments, to increasing economic distortions, raising tax rates disproportionately in certain sectors, or shifting tax burdens from corporations to noncorporate businesses or to individual investors. It is clear that the current corporate tax code needs to be improved to promote U.S. living standards and competitiveness. The challenge will be agreeing on a reform that levels the playing field across different industries and different investments in the face of the competing need to maintain revenues.

Fact 12: Addressing the deficite will require policy solutions equal to the size of the problem.

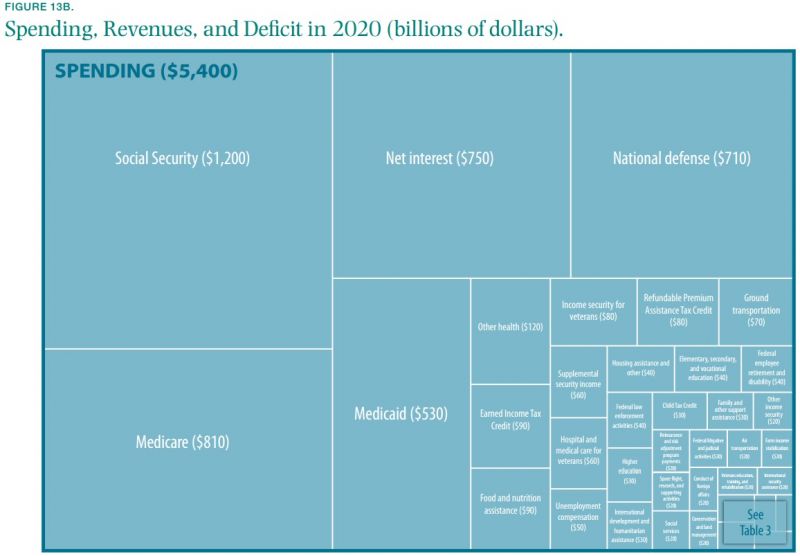

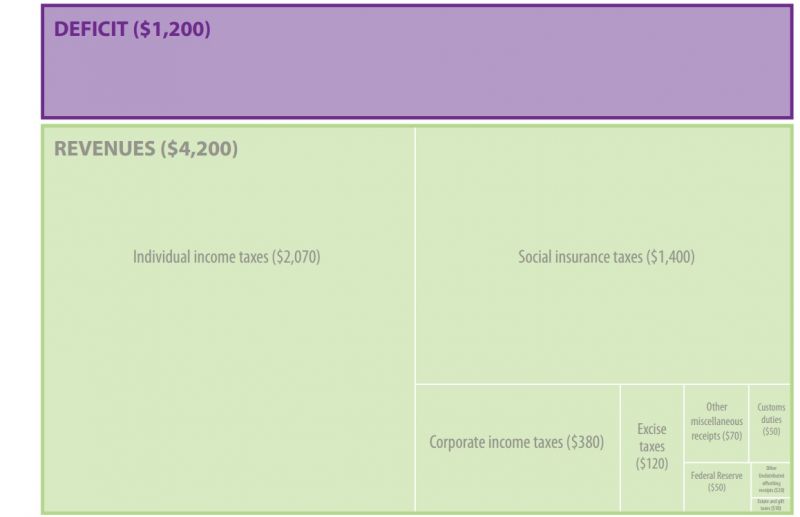

In 2020, the U.S. government will spend roughly $1.2 trillion more than it receives in revenues (CBO 2012b, alternative fiscal scenario). Addressing a budget deficit of this size will demand difficult trade-offs and require bold policy decisions. Nonetheless, we do not have a choice as to whether we would like to confront this challenge: budget deficits are projected to grow into the future, and America is on an unsustainable path.

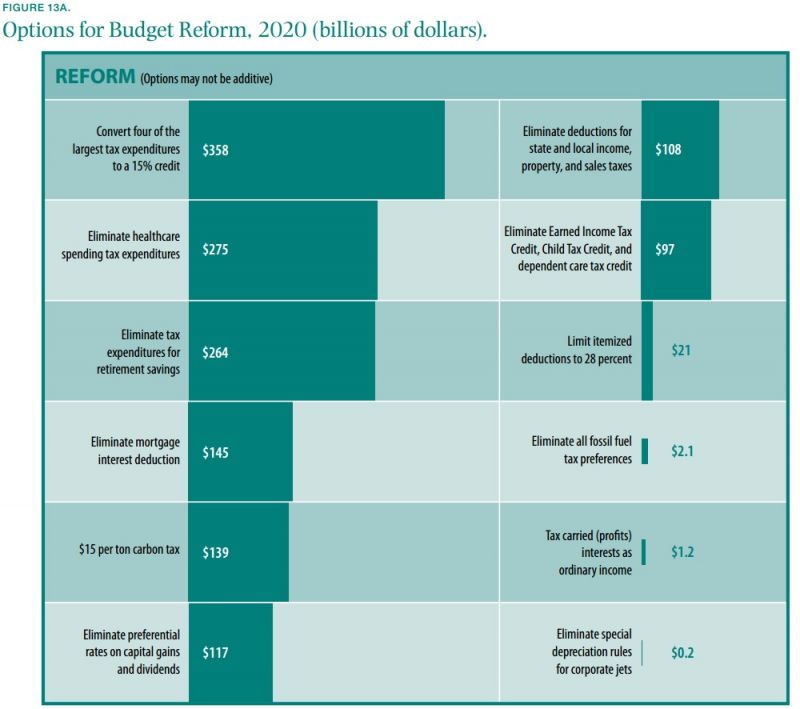

Figure 13 provides context for the ways in which many of the options discussed throughout this document fit into the broader budget debate. The figure illustrates individual spending and revenue components of the projected 2020 budget. Each rectangle represents one segment of the budget, with its area scaled according to the dollar amount of the expenditure or revenue. In addition, the figure provides a sample menu of policy options for addressing the deficit, each represented on the same scale. Changes in future economic conditions will have some effect on these items. For example, the projections assume that interest rates stay low for a few more years and then rise, but if interest rates continue to stay low, then the government’s net interest payments will be reduced.

Source: CBO (2012a, 2012b); OMB (2012). Note: Baseline is the alternative fiscal scenario. Figures 13A and 13B are drawn to the same scale.

Source: CBO (2012a, 2012b); OMB (2012). Note: Baseline is the alternative fiscal scenario. Figures 13A and 13B are drawn to the same scale.Certain budgetary items—such as foreign aid and the taxation of carried interest—garner frequent mention as targets for deficit reduction. But these policies are often referenced because they are easy targets, and not because they will actually resolve our budgetary issues. In fact, they are not nearly large enough to do so. For example, eliminating the special depreciation rules for corporate jets—a favorite example of some—would close the deficit by only $162 million in 2020, or roughly 0.01 percent (one-hundredth of 1 percent).

Big changes that could really chip away at the deficit would also entail complex considerations about how they affect progressivity, spending, and competitiveness. Eliminating the EITC, CTC, and DCTC, for example, would raise $97.4 billion in 2020, but also would allow more than 6.6 million people— half of them children—to fall back into poverty. This policy decision would help address the budget gap, but would leave in its wake a far less progressive tax system and greatly reduced incentives for low-income Americans to contribute to the economy through work.

As we consider the impacts that our decisions will have on the budget, on progressivity, and on American competitiveness, it is important to consider how the pieces of the policy puzzle fit together.