Although an expected slowdown in the labor market is anxiety-inducing, a slowdown is necessary to achieve stable inflation. We expect this slowdown to be marked by a temporary and modest increase in the unemployment rate above the level consistent with a sustainable pace of hiring. Viewed in the context of past business cycles, that would comprise a soft-ish landing and would constitute a remarkably swift return to a healthy economy.

Recent economic projections from the Congressional Budget Office and members of the Federal Open Market Committee (FOMC) are roughly consistent with a soft-ish landing. There remains considerable uncertainty about how the current slowdown will unfold. Nonetheless, returning to low and stable inflation with only a modest slowdown in economic activity and a modest increase in the unemployment rate would be a very good outcome relative to many possible alternatives.

Returning to low and stable inflation with only a modest slowdown in economic activity and a modest increase in the unemployment rate would be a very good outcome relative to many possible alternatives.

The gains in payroll employment have averaged 351,000 over the last three months, far in excess of the pace the labor market can sustain. In particular, given population growth and long-term trends in labor force participation, the stable pace of monthly increases in employment is roughly 70,000. Our concern is primarily forward-looking and less about the degree to which the pace of hiring has been a factor behind the recent increase in inflation. In absence of structural changes in labor market dynamics, gains well in excess of 70,000 are not sustainable without rising price inflation to help firms pay for accelerating wage growth.

Another aspect of the unsustainably hot labor market has been the very low rate of unemployment. Even though economists don’t know for certain the level of the aggregate unemployment rate that is consistent with stable inflation, several factors suggest that rate is higher than the current level of roughly 3½ percent. The unemployment rate has typically been low when the rate of job openings has been high; so, the low rate of unemployment partly reflects the temporary and unsustainable level of job openings. One way that a hot labor market can temporarily push the unemployment rate down is by shortening the period of job hunting, as firms use financial incentives to entice people to cut short their search.

Examining long-term trends in the unemployment rate, CBO estimates that the noncyclical unemployment rate is roughly 4¼ percent—varying modestly as demographics change over time. To the degree that an unemployment rate of 3½ percent is inconsistent with a stable labor market, it is also likely to be inconsistent with stable inflation—whether that is stable inflation at the Fed’s target of 2 percent or even somewhat higher at 3, 4, or 5 percent. To stabilize inflation (and bring it down to the Fed’s target of 2 percent), the labor market will need to soften to a sustainable pace.

In our view, the persistence of both high inflation, strong consumer demand, and very high job openings suggest that the Fed needs to slow the economy enough to open a modest amount of slack.

In our view, the persistence of both high inflation, strong consumer demand, and very high job openings suggest that the Fed needs to slow the economy enough to open a modest amount of slack. Not doing so risks inflation expectations rising to such a persistent degree that significant economic weakness would be necessary to bring inflation down. This will require the unemployment rate being temporarily above the noncyclical rate—which is itself somewhat higher than the current unemployment rate.

Previous analysis from The Hamilton Project suggests that a slowdown in job openings to a more stable rate would mean a temporary return to labor market conditions last seen around late 2014 and early 2015, when the unemployment rate was roughly 5½ percent. Similarly, in both the FOMC and CBO projections, the increase in the unemployment rate required to contain inflation is quite modest and the period in which the unemployment rate exceeds the noncyclical rate is short-lived. That outcome is made more likely by the relative stability in long-term inflation expectations, meaning that the Fed will not need to weaken the economy significantly in order to bring expectations back down.

The differences between a soft, soft-ish, and hard landing

With an unqualified soft landing, inflation would stabilize at the Fed’s 2 percent target and the unemployment rate would not rise above the rate consistent with a stable labor market. A soft-ish landing is one where inflation continues to fall back toward 2 percent but not without a modest weakening in the economy relative to its sustainable amount of activity.

In contrast, in a hard landing the economy weakens significantly relative to that sustainable amount. This would be evident from a large degree of slack, likely characterized by a sharp and perhaps persistent increase in the unemployment rate.

Current projections in a longer-term context

On February 15, CBO published its economic projections for the next decade. On March 22, the FOMC published its regular report showing the median of its members’ short- and long-run projections of the unemployment rate, inflation, and GDP growth.

As shown in figure 1, both the FOMC and CBO projections for the unemployment rate through 2025 show a temporary and modest softening in the labor market. CBO projects the unemployment rate will rise from its current level of 3.6 percent to 5.1 percent, before falling back about ½ percentage point toward a level consistent with stable inflation. The Fed anticipates a smaller increase, with the rate remaining below 5 percent, and a modestly lower unemployment rate consistent with stable inflation.

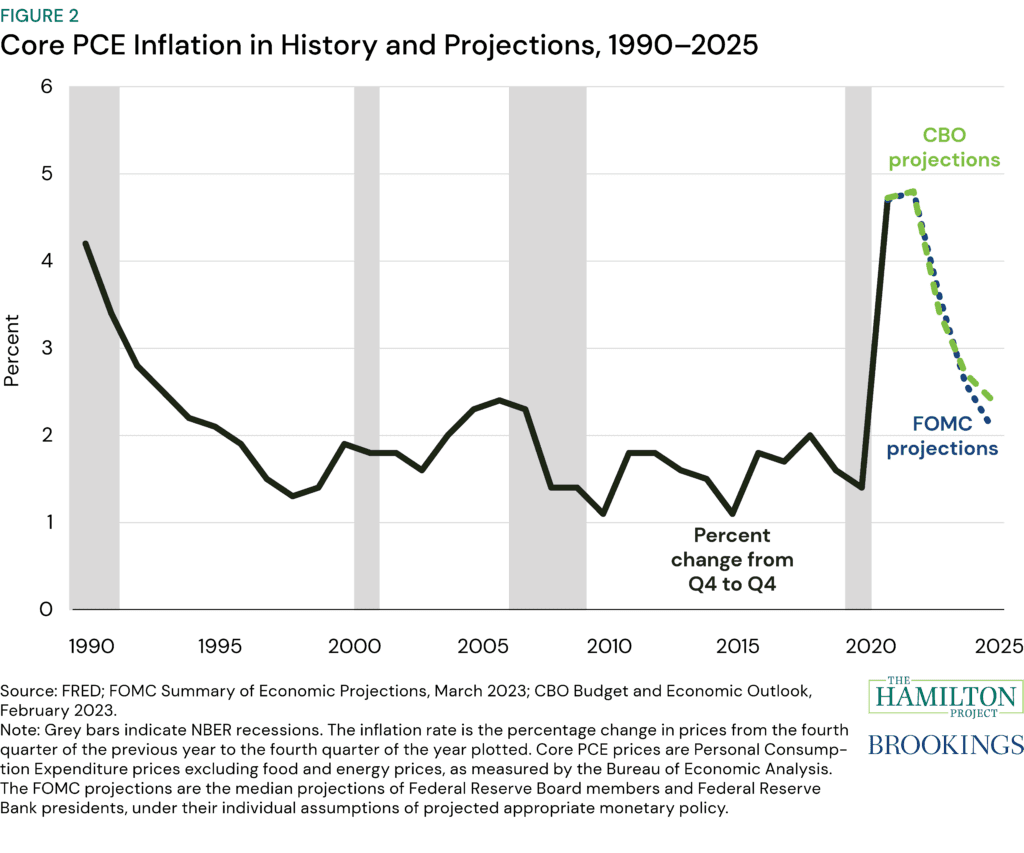

The Fed is more optimistic than CBO about how quickly the relatively modest slowdown in economic activity will bring inflation down to the Fed’s 2 percent target (figure 2). In CBO’s projection, core PCE inflation falls from roughly 4¾ percent in 2021 and 2022 to 3.4 percent this year and below 2½ percent by 2025 (on a Q4/Q4 basis). In the median projection from FOMC members, core PCE inflation falls to 3.6 percent this year and then to just above 2 percent by 2025.

Our expectation is that inflation can fall at that pace without prompting an increase in long-term inflation expectations. That allows policymakers to be somewhat patient. In other words, policymakers can continue to shoot for the soft-ish landing.

CBO’s and the Fed’s projections generally show real (inflation-adjusted) GDP moving sideways in 2023 and then resuming its upward trajectory in later years (see figure 3). With the historical context since 1990, one can see this slowdown is considerably more modest than the previous two recessions and less protracted than the recessions in the 1990s and early 2000s.

Conclusion

Of course, the soft-ish landing of these projections are not preordained; there are myriad risks that the United States’ economy could face in the next several years that would alter these projections. The Fed could over-tighten, leading inflation to undershoot its target, or it could tighten more quickly than necessary, squandering the chance for a soft-ish landing and creating significant albeit temporary weakness in the labor market. Alternatively, the Fed could tighten too little, perhaps under-appreciating the inflationary pressure from strength in certain parts of the economy even as other parts of the economy weaken.

For example, the recent failures of two regional banks and emergence of strains in the financial system have worsened the economic outlook. At the same time, house prices and new home construction have weakened considerably because of higher interest rates, and vacancy rates in commercial real estate have remained high. In contrast, consumer spending on goods, after accounting for inflation, has remained quite strong and is still more than 4 percent above trend. Such inconsistencies across the economy make the Fed’s job harder.

Any increase in the unemployment rate inflicts economic pain on the people who want a job and can’t get one. However, unexpectedly high inflation also inflicts economic pain as it eats away at the real value of wages and financial resources. The Fed’s efforts to maintain low and stable inflation will ultimately improve families’ financial security.