Every month for the last year, the Bureau of Labor Statistics’ wage data releases have continued to demonstrate that workers simply aren’t getting ahead. Despite some nominal growth, real wage growth has been consistently hovering around zero (rising at just a 0.2 percent annual rate from 2016-2017).

At the same time, this year’s annual data release from the Census Bureau showed us that the median household income has risen to $61,370 in 2017, a 1.8 percent increase even after adjusting for inflation.

How are real incomes rising even as real wages are flat? The answer lies in the simple fact that both hours worked and employment have been rising consistently. Annual income depends not only on wages, but also on the number of hours a person works in a year and the share of the population that is working.

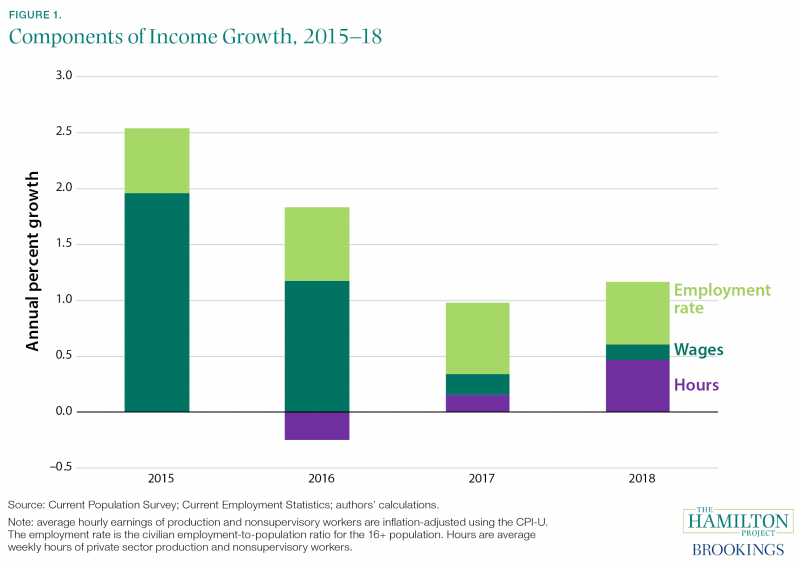

Figure 1 tracks these components of annual income over the last few years, scaling up the changes for 2018 to take into account the lack of data for September through December:

- In 2015 and 2016, low inflation contributed to strong real wage growth, which in turn supported household income growth.

- In 2017, and thus far in 2018, inflation has been higher, and while nominal wage growth picked up some, it has not increased enough to offset higher inflation. Thus, real wage growth has been close to zero, providing almost no boost to incomes.

- In 2018, increasing hours worked have been contributing to income growth.

- Throughout the 2015-2018 period, increasing employment as a share of the population has been supportive of income growth.

The rise in the employment rate is itself due to a set of underlying factors. First, the aging of the population—and increasing retirements—has put downward pressure on labor force participation. Second, an improving economy has meant that since about 2015, the labor force participation rate of prime–age workers has been increasing, and older workers are also staying in the labor force longer. Finally, a falling unemployment rate means that a higher share of those in the labor force have jobs.

Some of these factors can be predicted with a degree of certainty. In particular, the population will continue to age, and it is unlikely that the unemployment rate will continue to fall much below its current level of 3.9 percent. This means that, for rising employment to continue to support income growth, more of the people currently out of the labor force must enter the labor market. On that score, it is perhaps a worrying sign that prime–age participation has fallen below its recent February 2018 peak.

It is important to recognize that there are numerous other factors that contribute to changes in median household income. Changes in inequality may cause average income to behave differently than median income. We have tried to take this into account by using estimates of wages and hours for production and nonsupervisory workers, a group which roughly represents the bottom 80 percent of the wage distribution (and often mimics trends in median wages).

In addition, the number of individuals in a household can change, shifting median household income even when wages, hours, and the employment rate do not change. We have also used the most widely reported wage series—one that comes from a survey of employers (and consequently does not include self-employment income). If wages of self-employed workers move differently, this could affect household income without affecting employees’ wages and hours. Lastly, households receive income from sources other than wages (e.g., investment income). All of these complications can make it more difficult to derive household income from underlying growth in wages, hours, and employment.

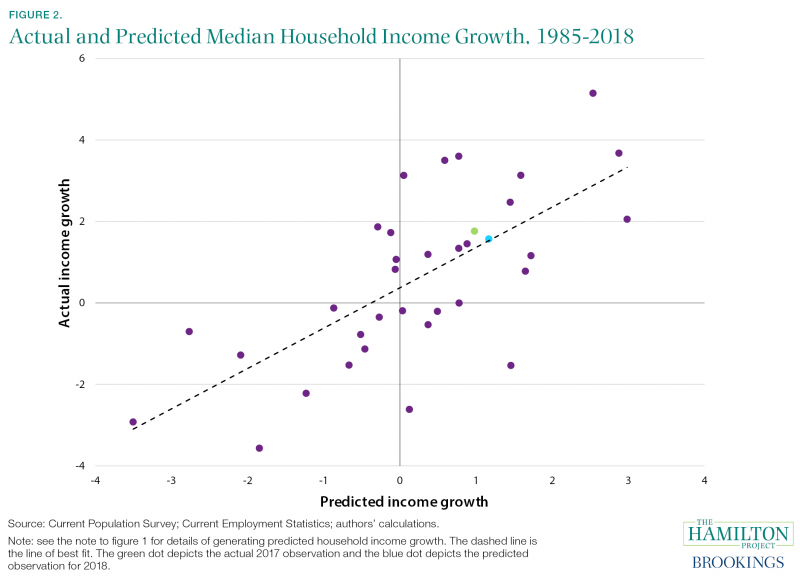

Given all these considerations, it may be surprising to learn that these three simple components when added together do a fairly good job of predicting the reported median household income growth.[1] Figure 2 shows the sum of growth in wages, hours, and employment on the horizontal axis and the growth in median household income on the vertical axis.[2] The dashed line shows the linear relationship between the two variables; in other words, it displays the predicted values of median household income for a given sum of wage, hours, and employment growth. While not all years lie directly on the line, we can account for roughly half of the variation in median income growth with this simple calculation. Had we performed this calculation at the end of 2017, it would have predicted median household income growth of 1.4 percent instead of the reported 1.8 percent.

Looking forward, available data for 2018 is consistent with median household income growth of 1.6 percent. For that to happen, though, either the employment rate must keep rising (as noted, perhaps an increasingly difficult outcome to achieve), average hours worked must keep rising, or real wages must start to grow more quickly through the remainder of 2018. Once there are fewer job seekers available to hire, real wages should experience additional upward pressure, but this has not yet occurred.

There are many other factors that will play a role in determining the household income growth rate for 2018. But given what we know today, it appears that household income is continuing to grow, albeit at a slower pace than a few years ago. In order to achieve more robust real income growth in 2019 and beyond, growth in real hourly wages will need to increase from its current pace.

Endnotes

[1] We use production and nonsupervisory hourly wages for wage data and total average weekly hours for hours data. Both series come from the Current Employment Statistics (the payroll survey of employers), a different survey than the Current Population Survey used to estimate household income. The different sources makes the predictive power all the more surprising. We use the CPI-U to adjust nominal wages for inflation, as this is the same price index used to calculate real median household income.

[2] CEA (2016) conducted a similar calculation using real average weekly earnings and employment to predict household income growth.