The recently released Trump Administration 2019 budget includes forecasts for economic growth that are substantially more positive than most private sector or other government forecasts. This allows the administration to project higher revenues and lower deficits than other forecasters—but reduces the value of the budget overall.

This is concerning given that economic growth forecasts are essential to determining whether the proposals in a budget actually add up. The budget must declare how the economy will perform in order to calculate revenue and (to a lesser extent, spending) estimates.

Furthermore, it is important to keep in mind that since spending and tax decisions originate in Congress, the President’s Budget is not immediately implemented as law. Instead, a President’s Budget is often seen as a vision statement outlining an administration’s priorities. Thus, creating a budget remains an important exercise given that it forces executive branch policymakers to publicly state how much they want to raise in revenue, how much they want to spend, and whether the revenues cover the spending.

Accordingly, one could imagine that if an administration were to use forecasts wildly out of line with plausible growth estimates to generate revenue, it would enable them to avoid making the hard choices on how to allocate and pay for their budget priorities. Regrettably, it appears that this is exactly what the Trump Administration has done with its FY19 Budget Request, considering:

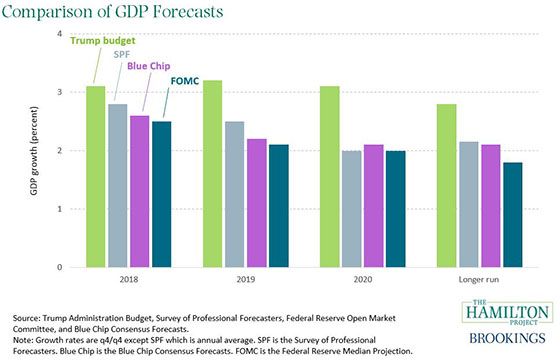

- The most recent estimates by members of the Federal Reserve Open Market Committee suggest that GDP growth will be 2.2 percent per year over the next 3 years and 1.8 percent in the long run.

- Blue Chip private sector forecasts are similar, at roughly 2.3 percent growth per year over the next three years (January forecast) and 2.1 percent in the long run (October forecast).

- The Survey of Professional Forecasters project 2.4 percent growth per year over the next 3 years and 2.15 percent in the long run (February forecast).

Yet the Administration’s forecast is notably higher, especially after 2018 (see figure), at 3.1 percent per year over the next three years and 2.8 percent over the long run. This is 0.7 percentage point higher over the next three years and 0.7 percentage point higher over the long run.

While the percentage points may seem small, these differences in forecasts have massive budgetary implications. In fact, the Office of Management and Budget estimates that GDP growth one percentage point lower than forecast would increase the cumulative deficit by over three trillion dollars over ten years.

Why is it unlikely that the United States will achieve the level of growth projected by the Trump Administration? The workforce is projected to grow about 1 percentage point slower in the next decade than it did in the 1980s, and half a percentage point slower than in the 1990s. Because GDP depends both on workforce and productivity growth, for GDP to grow roughly at the rate of the 1980s and 90s (3.2 percent) would require very high productivity growth, not just a rebound to its historical average growth rate, but growth even faster than during the productivity boom of the late 1990s. An increase in labor force participation could help, but it would only add 0.1 to 0.2 percentage points to growth over time, nowhere near enough to close this gap.1

Could the administration’s projected growth happen? Certainly. Is it the midpoint of a range of reasonable forecasts? No.

Because the budget forecasts are supposed to reflect the administration’s policy proposals, they may in fact differ from other forecasts that do not assume that many of its proposals will be implemented. However, the tax proposal has been law for a number of months and its general outline has been known for even longer. Recent budget deals may have allowed a bit more spending than others have forecast, but this would only affect economic growth for the next year or two, and not over the longer run.

It is certainly possible that growth will exceed expectations. Technological shifts, changes in propensities to work, and other relevant factors all follow paths that are difficult to forecast. Given the recent fiscal boost and the volatility of GDP growth from year to year, growth of 3 percent this year or next is certainly possible.

But, the general principle of budgeting is that one should use a reasonable estimate of costs and revenues. By selecting a growth forecast so far outside the mainstream, the Trump Administration is effectively betting the house on a very long-shot outcome. While this may not affect the long-run finances of the government, it does reduce the utility of the budget document itself. By assembling their proposals against an unrealistic backdrop, the administration appears to be abdicating it responsibility to fully consider the impact and ramifications of the tax cuts combined with the spending priorities and allocations within the FY2019 Budget Request.

1 See Jay Shambaugh, “How Fast Can We Grow – and Why That Matters” in Economics and Policy in the Age of Trump, Chad Bown ed. VOXEU, 2017.