Many American households are in a precarious financial position, leaving them potentially vulnerable to common changes in their finances such as a layoff. For example, in a typical year, 1.2 percent of workers are laid off through no fault of their own, and lower-paid workers are at higher risk of layoffs. Despite how common financial shocks are, only 63 percent of households had enough cash or equivalent saved to cover an unexpected $400 expense, and just 54% of households had enough savings to cover three months of routine expenses in 2023.1 Both household income and savings are crucial to helping households weather financial disruptions.

The U.S. safety net is intended to help individuals who are experiencing financial hardship. Households can become eligible for safety net programs when events occur that result in unexpected changes in household finances. These programs help households cover basic needs so that they may recover faster. Additionally, these programs are intended to provide a floor for necessities, such as food and medical care, for households in difficult financial circumstances.

The Supplemental Nutrition Assistance Program (SNAP) is central to the U.S. safety net’s ability to help families weather financial shocks. SNAP is a particularly important program because it is the only nearly universal means-tested program, meaning many low-income households are eligible, regardless of their demographics. In this piece, we show that SNAP not only helps recipients meet one of their basic needs, nutrition, but it also can help families withstand financial shocks.

What is SNAP, and who is eligible?

SNAP provides benefits to purchase groceries via a debit card at participating retailers. These “cash-like” benefits and their widespread availability mean they can be particularly useful in helping families steady their finances. In April 2023, the average monthly household-level SNAP benefit among beneficiaries was $343.

Most SNAP recipients spend more on food than the SNAP benefit amount, suggesting that, in absence of SNAP benefits, households would spend roughly the same amount in total on food. SNAP then frees up income that would otherwise have been spent on food for other necessities, such as housing, transportation, and child care. Thus, even though SNAP benefits come with more restrictions than cash, because they are spent on a basic need, the benefits help people handle unexpected changes in the rest of their budgets.

SNAP eligibility is largely independent of the demographics of the household and whether someone in the household works, which makes SNAP unique in the landscape of U.S. safety net programs. Generally, households are income-eligible if their income is below 130 percent of the Federal Poverty Level. In 2024, the poverty line for a household of three is $25,820 in the 48 contiguous states and D.C.

SNAP asset tests

Some households may additionally need to meet asset tests to be eligible for SNAP, which, in principle, could discourage savings among these households so that they remain eligible. If someone resides in one of the states that still has asset tests, this means that the value of individuals’ liquid assets (savings and checking accounts) and property assets (vehicles and homes) must be under a certain threshold in order to be eligible. In 2023, the federal liquid asset limit for working-aged households was $2,750. However, as of 2024, only Alaska, Arkansas, Idaho, Indiana, Kansas, Mississippi, Missouri, Nebraska, South Dakota, Tennessee, Texas, Utah, and Wyoming still use asset tests to determine SNAP eligibility.2

We find, using the Survey of Income and Program Participation from 2013 to 2016, that the median liquid asset value among those income-eligible for SNAP (regardless of whether they receive SNAP, or live in a state with asset tests) is only $141 in 2023 dollars. That amount is far less than that typically deemed necessary to cover a surprise expense. In comparison, households with income above the SNAP income-eligibility threshold have a median liquid asset value of $6,382.

These statistics also imply that most households who are income-eligible for SNAP have assets well below the asset test threshold, so the liquid asset test has little value in terms of impacting program targeting. This is of further significance since prior research has found that asset tests increase program churn and administrative costs because they require burdensome paperwork and cause confusion about program rules that deter some eligible people from receiving benefits.

What resources do SNAP households have to cover financial hardship?

To further investigate if households who are likely eligible for SNAP can weather unexpected changes in their finances on their own, we explore whether and how households would be able to pay for an unexpected $400 expense by households’ annual income. In general, $400 is a relatively low amount for routine unexpected expenses; for example, the average cost of an unexpected car repair is $500-600, getting a car towed can cost up to $600, urgent health care visits cost up to $200, and hospital emergency room visits can cost up to $1,300.

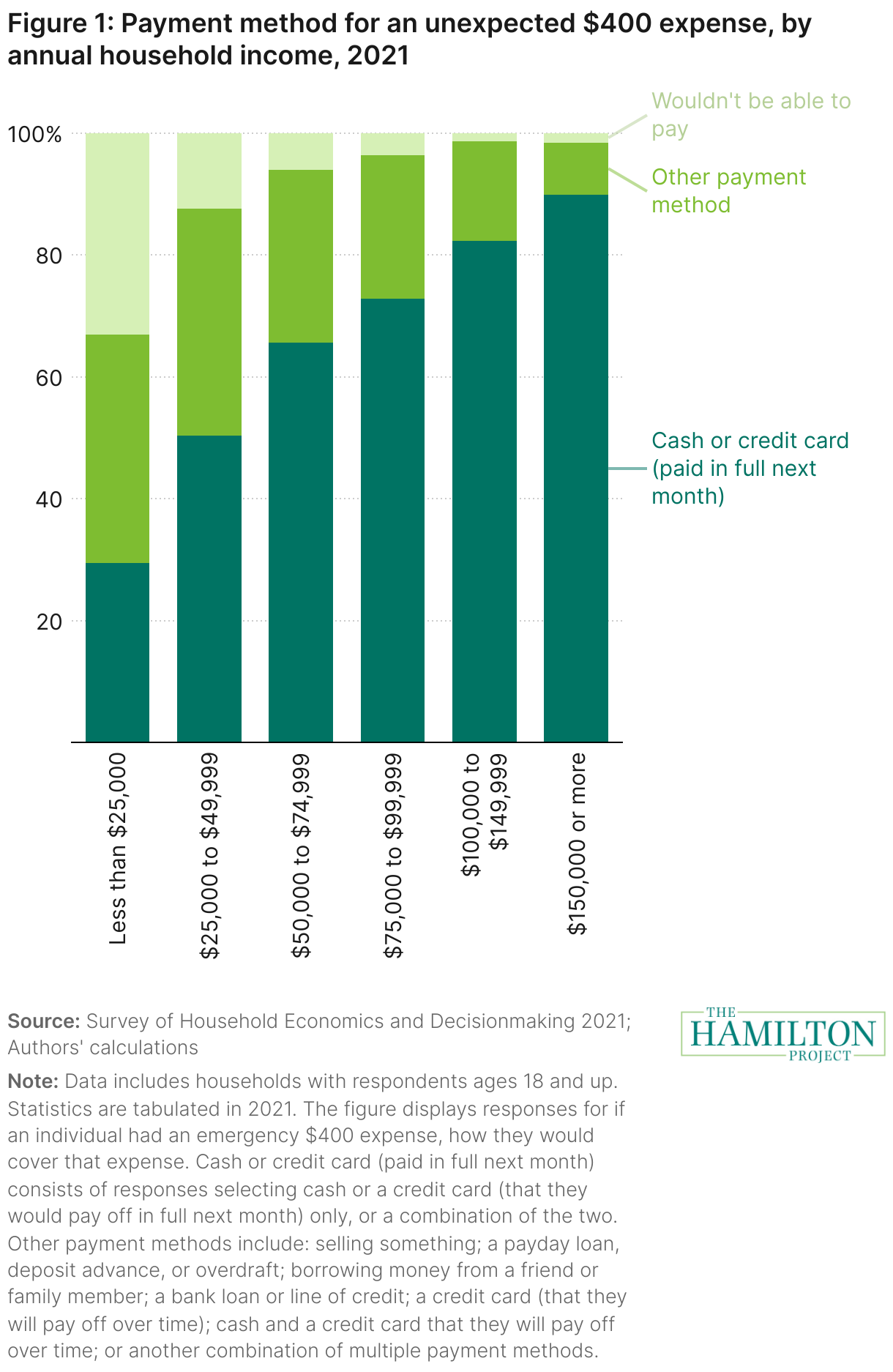

Figure 1 shows this analysis using the Survey of Household Economics and Decisionmaking (SHED) data from 2021. The SHED data offers household income information in bins, with the lowest bin being households with less than $25,000 in annual income. Many of these households, though not all, will be eligible for SNAP. We focus on households who are likely eligible for SNAP, rather than those receiving SNAP, since who receives SNAP depends on other household circumstances that may also affect the household’s financial situation.

For households with annual incomes below $25,000 (most likely eligible for SNAP), only 29 percent can cover an unexpected $400 expense using cash or a credit card that they will pay off immediately (savings-reliant methods). This is compared to 50 percent of those with income between $25,000 and $50,000. The ability to cover an unexpected expense of $400 using savings steadily increases with household income, and the highest income households—those with annual income over $150,000—are almost all able to cover such an expense with liquid savings (90 percent).

Without resources on hand to deal with unexpected changes in their budgets, households can face harmful financial repercussions. For example, many of those who have low savings report that an unexpected expense or loss in income would subsequently cause them to miss payments on other necessary expenses such as housing and utility bills, and, in some cases, this leads to eviction. It is also important to note this can lead to persistent negative financial outcomes—for example, missed utility and rent payments can negatively affect credit scores.

Households turn to SNAP to help weather unexpected changes in finances

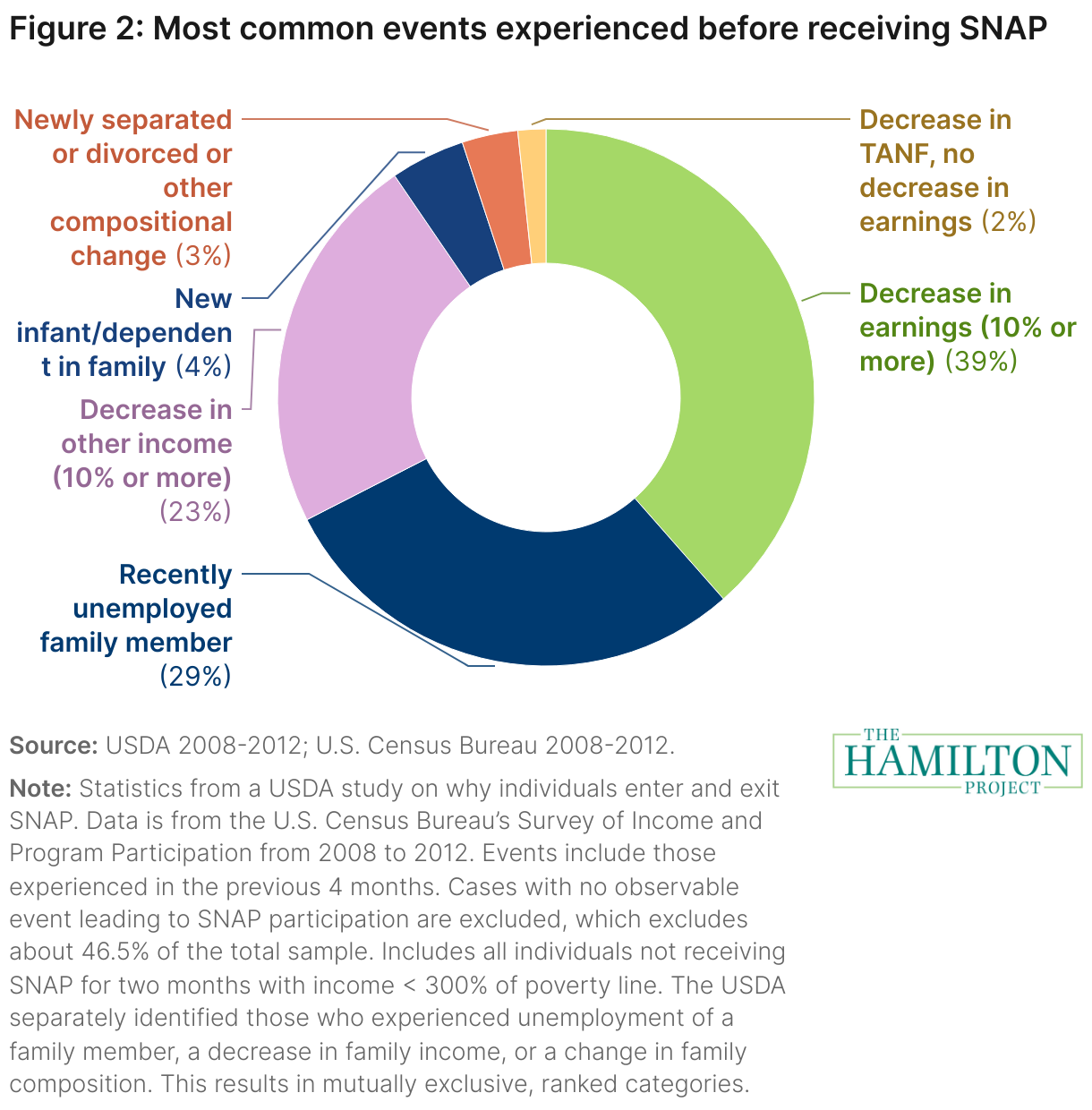

Households turn to SNAP when they are in financial distress. Analysis by the USDA of SNAP participants in 2008–2012 found that many new SNAP recipients experience a reduction in income in the months before beginning SNAP receipt. Figure 2 shows the most common events in the four months preceding new SNAP participation, among those with an observable event. For 29 percent of new SNAP recipients, an adult in the household became unemployed. An additional 62 percent of new recipient households experienced a loss in income of more than 10 percent before receiving SNAP. The other most common precipitating events are changes in household composition, such as a new child in the household.

This is consistent with other research by one of the authors of this piece which studies the earnings and employment of SNAP applicants in 2012–2016. This research finds that some SNAP applicants experience a drop in earnings and employment around the time they apply for SNAP. Importantly, this drop is present whether or not the applicants eventually receive SNAP, suggesting it is due to external events, such as layoffs, and not due to a strategic change in finances in order to qualify for SNAP.

Recent research finds that limiting access to SNAP increases credit inquiries and credit usage, so when households cannot use SNAP to help weather a financial shock, they turn to other methods to cover their spending. Importantly, limiting access to SNAP increases the likelihood of past-due balances on credit, indicating financial distress. Thus, access to SNAP reduces reliance on borrowing that may lead to other negative financial consequences because of late fees, high interest rates, and impacts on credit score.

SNAP, then, helps households balance budgets when facing financial distress, which in turn helps them keep up with rent and other important bills without facing harmful ramifications of credit usage.

Conclusion

SNAP plays a vital role in providing essential financial stability for low-income households who have little savings and face economic challenges. These challenges are common and generally happen through no fault of the households themselves—for example, being laid off from a job. SNAP is particularly important as insurance since it is the only major program in the U.S. that helps nearly all types of low-income households, regardless of demographics, weather financial challenges. This also helps households avoid costly borrowing and a cascade of related financial hardships such as missing housing and utility bills.

1. Options for paying the $400 expense include: a credit card, checking or savings accounts, cash, bank loan or line of credit, borrowing from a family member, payday loans, deposit advances, overdrafts, or selling something.

2. Asset tests have been largely eliminated through the implementation of broad-based categorical eligibility (BBCE)

Acknowledgements

We are grateful to Lauren Bauer, Wendy Edelberg, Robert Greenstein, Dottie Rosenbaum, Joseph Llobera, and Marie Wilken for generous feedback.