The challenge

The U.S. corporate tax is at a crossroads. Originally designed as an income tax, it has been altered in several incremental steps—most recently, last year’s tax law—that move it partway to a tax on business cash flows. The resulting hybrid has major flaws.

While a true cash-flow tax has the advantage that it does not distort investment or financing choices, the hybrid system produced by recent legislation treats different forms of investment and financing differently, distorting investment decisions and creating tax avoidance opportunities. Particularly problematic, the 2025 tax law made expensing (immediate deductibility) permanently available for most forms of corporate investment, while preserving and expanding deductions for corporate interest payments. The result is that effective tax rates on debt-financed investments are often negative, i.e., a firm makes more money from its investment because of the tax system. Negative tax rates invite the development of new tax shelters, distort businesses’ choice of how to finance investments, and can even lead to wasteful investments made just for tax reasons.

The potential for profit shifting and a plethora of special interest loopholes only add to these problems. Corporate income is taxed based on where firms produce rather than where they sell, creating incentives for firms to shift profits out of the country. At the same time, dozens of narrow, targeted incentives are of questionable effectiveness, narrow the tax base, introduce distortions and complexity, and reduce U.S. revenues. In part due to the proliferation of tax subsidies and growing opportunities for profit-shifting, the long-run trend has been a decline in the revenue raising power of the corporate tax, even as corporate profits have risen as a share of GDP.

The proposal

William Gale (Brookings Institution), Adam Looney (Marriner S. Eccles Institute, David Eccles School of Business, University of Utah), and Elena Patel (Brookings Institution) propose to transition the current U.S. corporate tax to a border-adjusted cash-flow tax with a broad base by:

Converting the corporate tax base to a cash-flow tax base. The authors propose to complete the shift to cash-flow tax treatment of investment by allowing expensing for those categories of investment not already covered by recent legislation and eliminating deductibility of interest payments. These changes would set the effective corporate tax rate on new investment equal to zero, versus the current system under which these rates range from positive for certain investments to negative (i.e., tax subsidies) for most categories of investment if financed with debt.

Eliminating most targeted tax expenditures. The authors propose eliminating most targeted deductions, credits, and special regimes. While some such provisions may be adopted to pursue specific worthwhile policy goals, they introduce distortions and complexity that a cash-flow tax is otherwise designed to avoid.

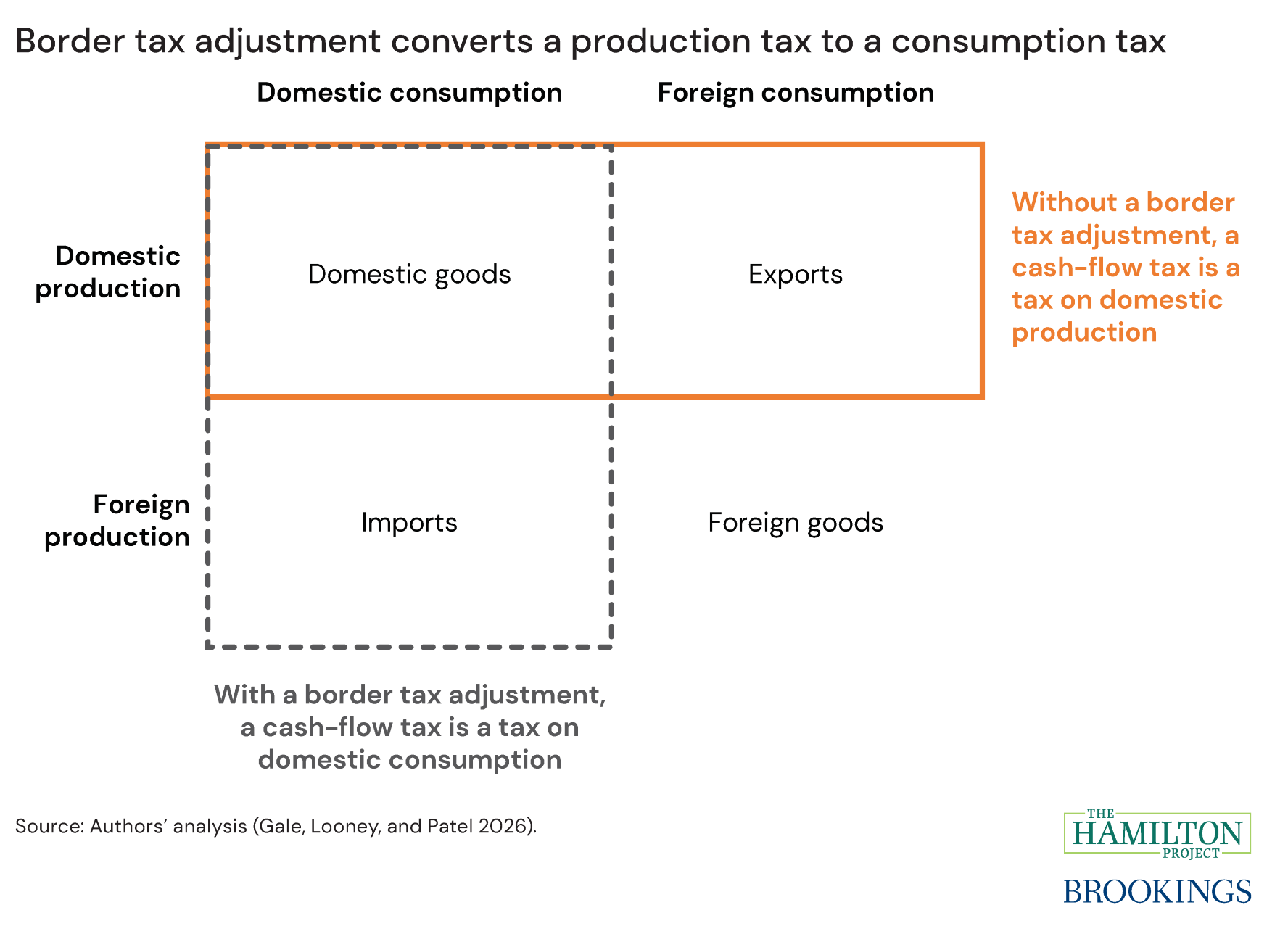

Border-adjusting exports and imports. Businesses would be taxed based on U.S. sales, rather than U.S. production: what is known as a border-adjusted cash-flow tax. Border adjustment largely eliminates profit-shifting incentives, insulates the U.S. corporate tax from the international “race to the bottom” in corporate income tax rates, and broadens the tax base and increases revenue capacity.

Raising the statutory corporate tax rate to 25 percent. Because the U.S. fiscal outlook shows a clear need for more revenue and because the reformed tax base would sharply reduce investment disincentives and other economic distortions from any given statutory tax rate, the authors propose to increase the corporate tax rate to 25 percent.

This package would increase investment, simplify the corporate tax, reduce distortions, and raise revenue in a progressive manner. The authors estimate that, taken as a whole, the proposal would raise over $4.7 trillion over 10 years. Even without the border adjustment, the domestic reforms alone would raise about $1.5 trillion over 10 years and make the corporate tax system simpler and more efficient, although they would not address profit shifting or international rate competition.