The United States collects substantially less revenue from corporations than it did several decades ago, and less than peer countries do today. These declines have contributed to rising deficits and to declining effective tax rates on capital income and high-income Americans.

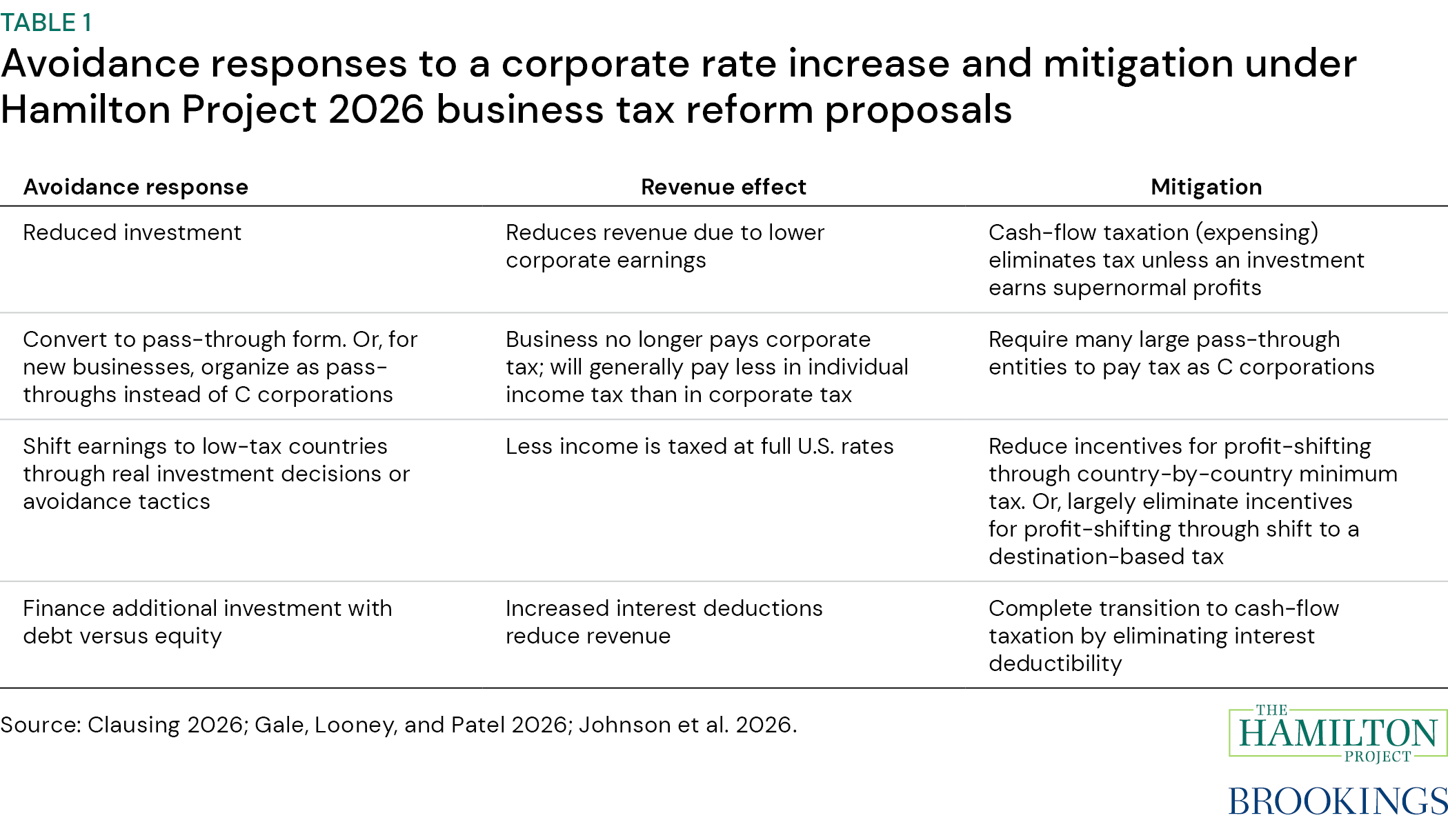

While strengthening individual-level taxes on capital income is also important, strengthening business taxes is a critical step toward a progressive tax system that meets national needs. Three new Hamilton Project proposals offer ideas to raise revenue from business tax reform. William Gale, Adam Looney, and Elena Patel propose to complete the transition of the U.S. corporate tax from an income tax to a coherent, destination-based cash-flow tax. Miles Johnson, Thalia Spinrad, Kathleen Bryant, and Chye-Ching Huang analyze a proposal to tax large pass-through businesses as C corporations. Kimberly Clausing proposes a package of corporate tax reforms that would raise the corporate tax rate, reform the tax base, and address the problem of international profit shifting by implementing a stronger international minimum tax, building on the multinational “Pillar Two” global corporate minimum tax agreement.

While each of these proposals could be adopted separately, aspects could be combined into a holistic reform that is more than the sum of its parts. In addition to its direct effects, such a reform would increase the revenue available and reduce economic distortions from raising the corporate rate. As an illustrative example, a combined reform that also increased the corporate rate to 30 percent could raise over $400 billion (0.9 percent of GDP) annually by 2035, based on Urban-Brookings Tax Policy Center and Penn Wharton Budget Model estimates, roughly reversing the decline in the corporate tax since the late 1990s.

Background

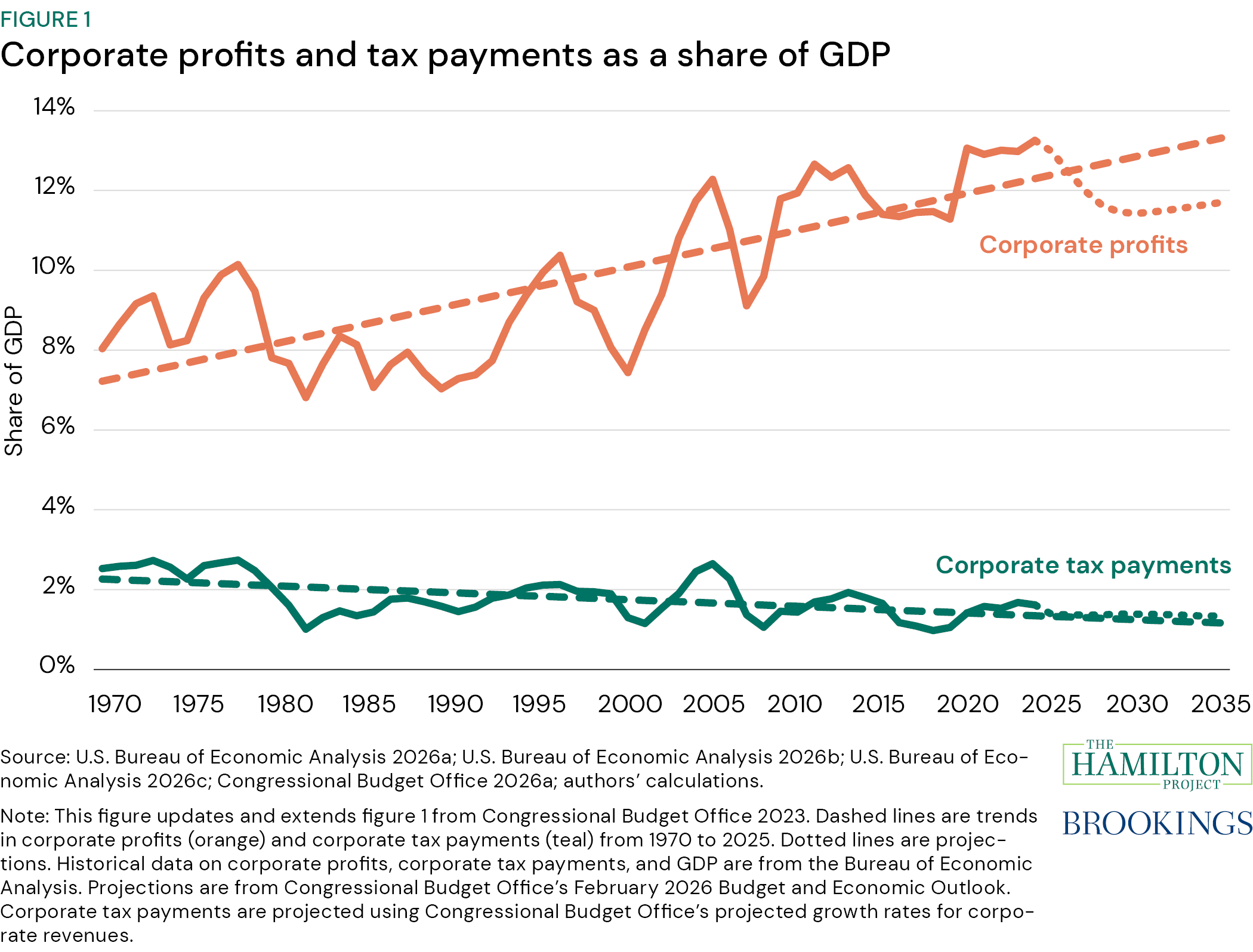

The United States collects substantially less revenue from corporations than it did several decades ago. The corporate tax, which raised an average of 2.6 percent of GDP in the 1970s, has raised that amount in only two years since. The Congressional Budget Office (CBO) projects that the corporate tax will raise an average of 1.3 percent of GDP over the coming decade, down from an average of 1.8 percent from 1980–2009 and 1.5 percent from 2010–25. Corporate receipts as a share of GDP have fallen even as corporate profits have risen sharply over the same period (figure 1).1

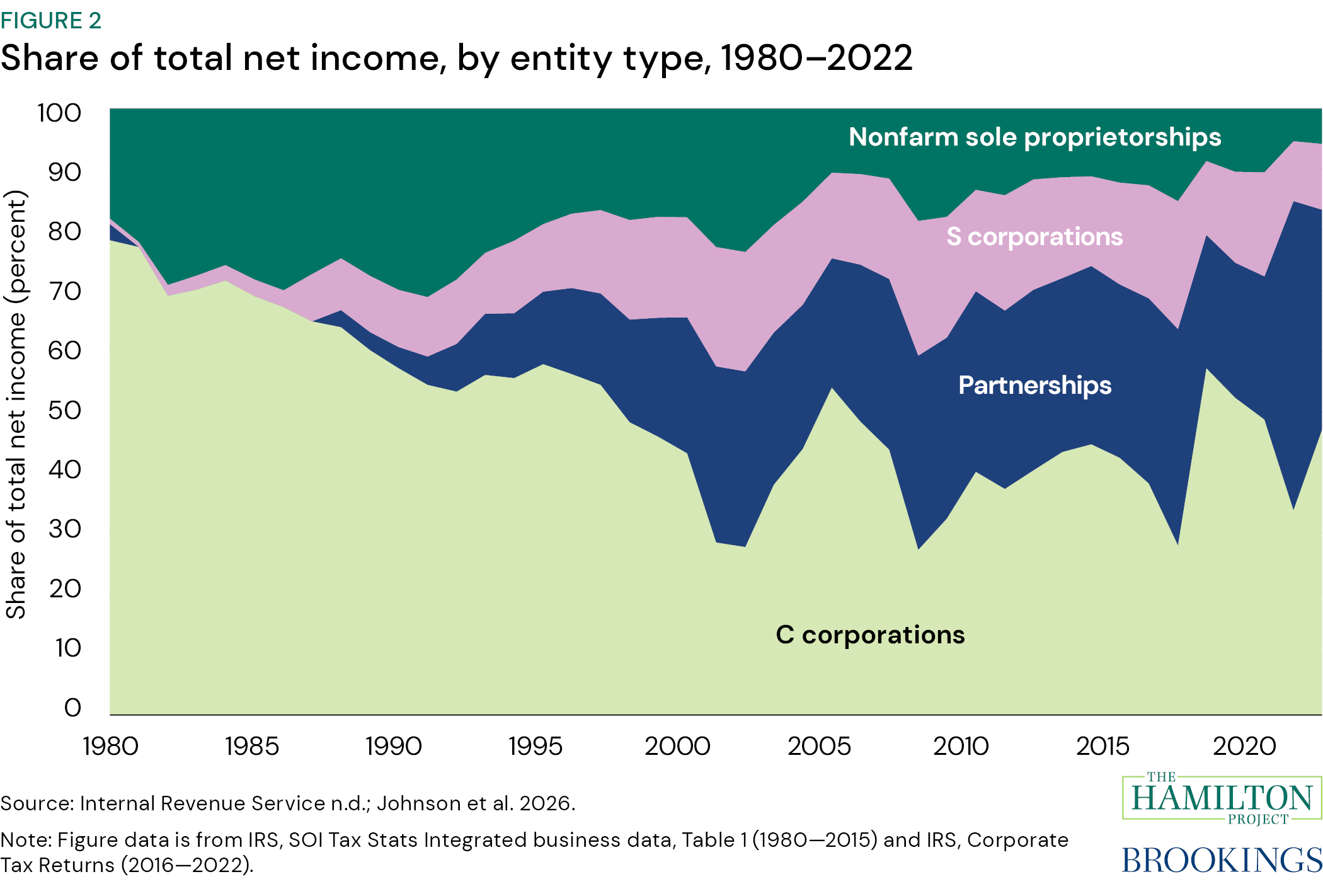

Some of the decline in corporate tax receipts, especially in the 1980s and 1990s, reflects changes in how businesses are organized. Instead of organizing as C corporations, which are subject to the corporate tax, more firms now organize as pass-through entities (S corporations, partnerships, and sole proprietorships), allowing owners to bypass the corporate tax and pay a single level of individual income tax on business income. There was a sharp increase in the share of business income earned in the pass-through sector following the 1986 Tax Reform Act, followed by continued growth, especially for partnerships, into the 2000s (figure 2).

Although the growth of the pass-through sector led to an increase in individual income tax receipts from businesses that offset some of the corporate income tax declines, overall, it reduced federal tax revenue. Pass-through businesses pay tax at lower effective tax rates, on average, than if they were organized as C corporations, the result of both the different statutory regimes and additional avoidance opportunities available to pass-throughs (Johnson et al. 2024). Moreover, pass-through entities are also used to recharacterize owners’ labor income as business income, resulting in lower taxes than if the labor income were treated as wages (see for example Smith et al. 2019).

Researchers have estimated that total federal revenues were about $76 billion (0.5 percent of GDP) lower in 2007 compared to if all pass-throughs were organized as C corporations and about $100 billion (0.6 percent of GDP) lower in 2011 compared to if the pass-through share of business income was the same as in the early 1980s (Congressional Budget Office 2012; Cooper et al. 2016). While the 2017 tax law reduced the corporate income tax rate, effective tax rates on pass-through income remain lower, on average, than effective tax rates on C corporations (Goodman et al. 2024; Pomerleau 2024).

Setting aside the growth of the pass-through sector, corporate tax receipts have also fallen sharply over time as a share of C corporation economic profits.2 Likewise, U.S. corporate tax receipts are low as a share of GDP compared to other developed countries, even though corporate profits, accounting only for C corporations, are high (Clausing 2026).

Besides the growth of the pass-through sector, other important contributors to declining corporate receipts include multiple rounds of legislated tax cuts. Of particular note, the 2017 tax law reduced the top corporate tax rate from 35 to 21 percent, and its business tax provisions were projected to reduce revenues by about $75 billion (0.4 percent of GDP) annually from 2018 through 2021, a period when most of the law’s policies were fully in effect (Joint Committee on Taxation 2017). The 2025 tax law enacted over $100 billion (0.3 percent of GDP) annually in business tax cuts over the decade from 2025 to 2034, including making permanent the 2017 law’s temporary expensing for most business assets (Committee for a Responsible Federal Budget 2025). (Expensing lets businesses immediately deduct the full cost of investments, rather than deducting the cost over time as an asset’s value depreciates.)

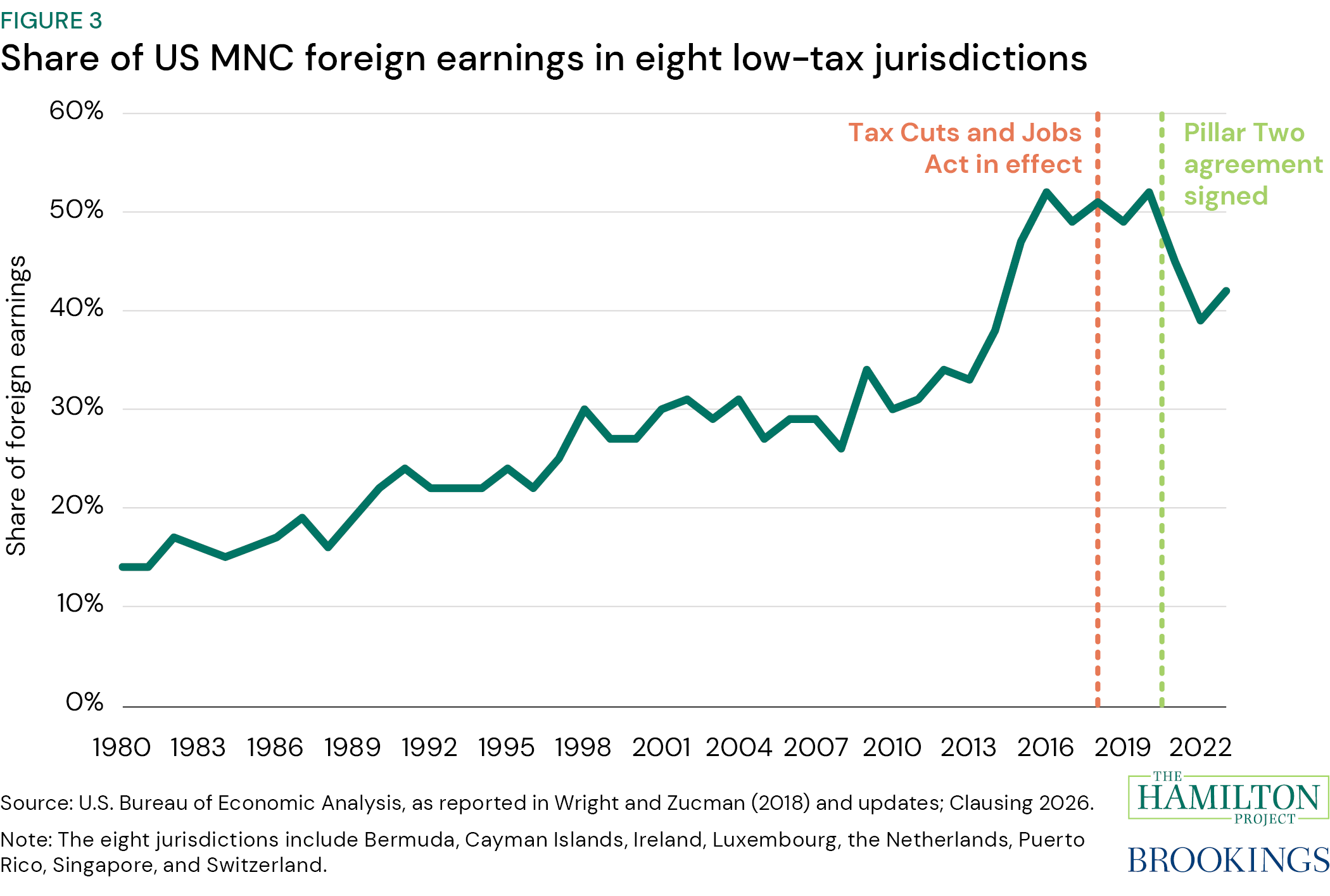

Finally, tax avoidance through shifting assets and profits to low-tax countries has increasingly eroded the corporate income tax base. As shown in figure 3, the share of U.S. multinationals’ foreign earnings reported in key low-tax countries grew rapidly in the late 1990s and the mid-2010s, remained high following the 2017 tax law, and remains high still despite declines following the Pillar Two international tax agreement discussed below (Clausing 2026). Clausing has estimated that revenue losses from international tax avoidance, small prior to the late 1990s, grew to over $100 billion annually (over 0.5 percent of GDP) by 2017 (Clausing 2020).

Why raise revenue from business tax reform?

Declines in business tax revenue increase the deficit and make the tax system less progressive, and reversing these trends is a critical step toward a progressive tax system that meets national needs.

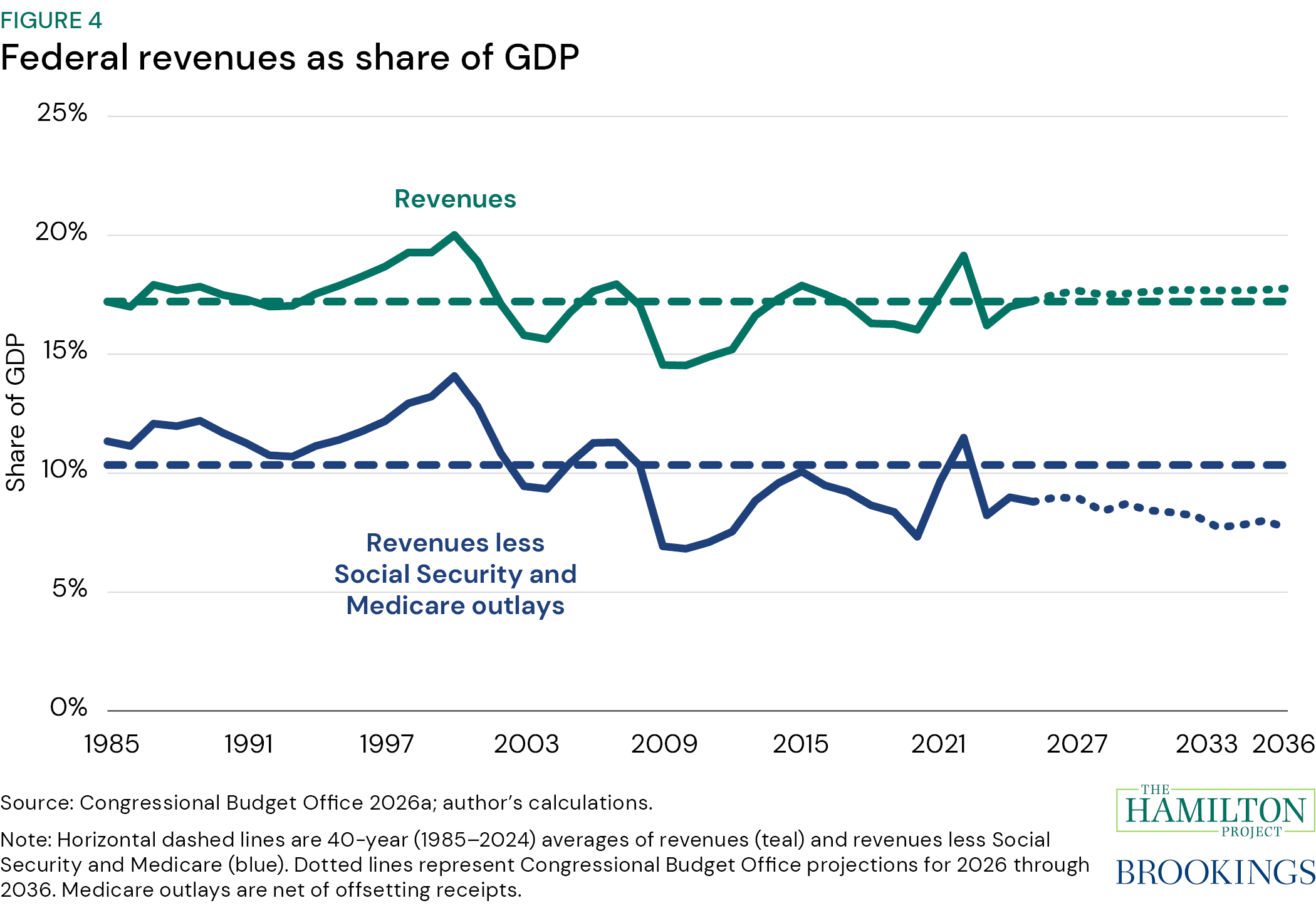

Falling revenue from any source is especially concerning at a time when fiscal pressures from an aging populating are growing. As figure 4 illustrates, while revenues in 2025 were roughly in line with their 40-year average as a share of GDP, revenues subtracting only Social Security and Medicare costs—in other words, the revenues available to cover everything else in the federal budget—were more than 1.5 percent of GDP (more than $450 billion) below the 40-year average.

The shrinking corporate tax has also contributed to declining tax rates on capital income and, relatedly, on high-income people. Overall effective marginal tax rates on capital (excluding land and inventories), as calculated by the Congressional Research Service, have fallen from 8.9 percent prior to the 2017 tax law to 5.4 percent following the 2025 tax law (Gravelle and Keightley 2025). The pre-2017 tax law rates were lower than in prior decades (Gravelle 2006).

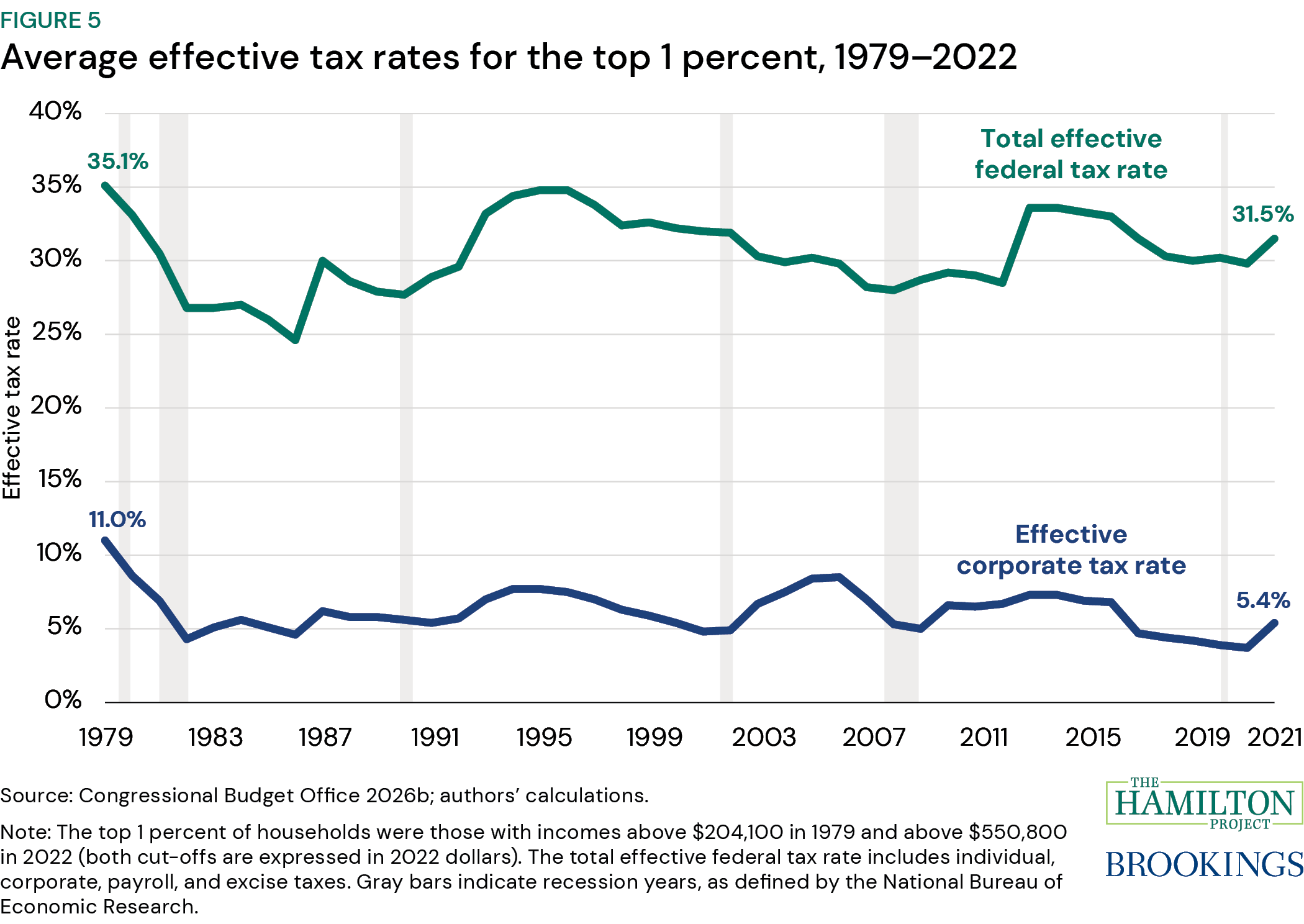

Meanwhile, falling corporate tax collections more than account for the drop in effective tax rates on the top 1 percent of households from 1979 through 2022. Over this period, this group’s total effective federal tax rate fell from 35.1 to 31.5 percent (a decline of 3.6 percentage points), while their corporate effective tax rate fell from 11.0 to 5.4 percent (a decline of 5.6 percentage points; Congressional Budget Office 2026b).3 (See figure 5.) Likewise, for the top 0.0002 percent (about 400 households), the drop in the corporate effective tax rate more than accounts for the drop in overall federal tax rates from 2010 to 2020. Over that period, this group’s total federal effective tax rate fell from 27.5 to 23.8 percent (a decline of 3.7 percentage points), while their corporate effective tax rate fell from 16.2 to 8.9 percent (a decline of 7.3 percentage points) (Balkir et al. 2025).4

This in turn reflects the fact that business income makes up a large share of top incomes. Balkir et al. (2025) find that business income comprised almost 85 percent of the total income of the very wealthiest (top 0.0002 percent, or about 400) American households from 2018–20. About a third of this group’s total income comes from investments in public corporations and about half from private businesses, with the rest coming from wages and salaries, carried interest, and capital gains not flowing from corporate retained earnings. A different but related set of calculations for the top 0.1 percent finds that business income made up nearly 60 percent of their income in 2014 (most from pass-through businesses), with the rest roughly evenly split between wages and other capital income (Smith et al. 2019).

Because business income—from both C corporations and pass-throughs—is such a large share of top incomes, the current tax system’s low rates and avoidance opportunities for business income severely limit its capacity to raise revenue from the highest-income groups. Conversely, comprehensive taxes on business profits could in principle be used to achieve policymakers’ desired level of taxes on the bulk of non-wage income flowing to very high-income groups.

Nonetheless, proposals to increase business taxes have been overshadowed in recent public debates by proposals to increase individual taxes on capital income. While strengthening individual-level taxes on capital income is also important, business tax reforms should be part of any revenue-raising effort because they avoid legal risk, build on existing tax administration infrastructure, and have the potential to reach substantial income that individual policies typically miss.

One key feature of business tax reforms is that they can raise substantial revenue without taxing unrealized capital gains. Unrealized capital gains account for a significant share of total income for high-income groups. The even bigger problem, however, is that non-taxation of unrealized gains provides an escape hatch from most other attempts to tax capital income at the individual level. Policies that increase taxes on other major forms of capital income (such as realized capital gains or dividends) will lead high-income people to shift more of their income into the form of unrealized gains, limiting what these tax policies can raise.

Recognizing this problem, policymakers have proposed a number of approaches to taxing unrealized capital gains. These include former President Joe Biden’s proposal for a 25 percent minimum tax on total income (including unrealized gains) for those with net worth over $100 million; Sen. Ron Wyden and Reps. Steve Cohen and Don Beyer’s proposal to require mark-to-market taxation of tradeable assets for those with annual income over $100 million or net worth over $1 billion; and wealth tax proposals from Sen. Bernie Sanders and Rep. Ro Khanna and from Sen. Elizabeth Warren, Rep. Pramila Jayapal, and Rep. Brendan Boyle, among others (U.S. Department of the Treasury 2024; U.S. Senate Committee on Finance 2025; Office of Sen. Bernie Sanders 2026; Office of Sen. Elizabeth Warren 2026).

Such approaches deserve serious consideration. But while legal experts have made strong arguments that taxes on unrealized gains are constitutional income taxes, many also see at least some chance that the current Supreme Court would strike down at least a wealth tax (see for example Batchelder and Kamin 2019; Liscow 2026). This risk counsels against relying entirely on these instruments to address the shortcomings of current U.S. taxes on capital income.5

In contrast, entity-level business taxes do not depend on solving the problem of unrealized gains, because they don’t provide the same escape hatch. If a business is subject to tax on its current profits, those profits will be taxed regardless of how it ultimately pays them out to shareholders.6

A related advantage of business tax reforms is that they can generally build on existing tax infrastructure. In contrast, wealth taxes or taxes on unrealized capital gains would require new rules and administrative capacity to tax non-publicly traded assets, which account for a substantial minority of high-net-worth individuals’ total wealth. While certainly a surmountable problem, valuing these assets would require significant new tax infrastructure; according them special tax treatment to avoid valuation problems could invite individuals to shift their wealth into this form.7

Finally, business and individual tax reforms each have the potential to reach capital income streams the other misses, suggesting they could be complementary. Individual-level taxes can reach the substantial capital gains not attributable to corporations’ retained earnings, for example, stock appreciation in anticipation of a company’s future profits. But individual-level taxes will often miss gains on the large share of U.S. company stock held by foreigners (more than 40 percent in 2022), as well as gains on stock held by nonprofits or in tax-exempt accounts (Rosenthal and Mucciolo 2024).

Moreover, partly as a consequence of the administrative complexities and associated compliance burdens, prominent proposals to tax unrealized capital gains target only the extraordinarily wealthy, with net worth thresholds ranging from $50 million for Sen. Warren’s wealth tax to $100 million for former President Biden’s proposal to tax unrealized capital gains income to $1 billion for Sen. Sanders’ wealth tax. These high-wealth groups account for eye-popping shares of wealth compared to their share of the population. Still, proposals that target only these groups would collect no additional revenue from the large majority of national wealth. For example, former President Biden’s proposed minimum tax, with the $100 million threshold, was estimated to apply to the top 0.01 percent of households; that group held on the order of 7 percent of U.S. wealth in 2016 (Smith et al. 2023). Business tax reforms that build on existing tax infrastructure can potentially reach a larger share of capital income and wealth.

Proposals for reform

Three new Hamilton Project policy proposals offer concrete business tax reform ideas that raise revenue by addressing substantive flaws of the current system.

The domestic corporate tax base. Gale, Looney, and Patel take stock of the corporate tax in the wake of the One Big Beautiful Bill Act (OBBBA) of 2025 and propose reforms that would raise revenue by completing the transition from an income tax to a cash–flow tax.

The economic attraction of a cash-flow tax is that, unlike an income tax, it generally does not discourage business investment. Under a cash-flow tax, investments that earn only a “normal” return—the rate of return available from investing the funds elsewhere—effectively pay no tax. That’s because, under a cash-flow tax, businesses can claim a deduction for the full amount of investments up front (“expensing”), and the associated tax benefits equal the present discounted value of the tax payments due on the normal return. As a result, tax rates are positive only on supernormal returns. Since investments that earn supernormal returns are worth making as long as the tax on these returns is less than 100 percent, a cash-flow tax should not reduce total investment.8

The OBBBA enacted permanent expensing for machinery and equipment, restored expensing of research investments, and introduced expensing on a temporary basis for some investments in structures, with the result that a large majority of business investment is now subject to cash-flow tax treatment. But, as Gale, Looney, and Patel point out, the U.S. shift toward a cash-flow tax is incomplete, resulting in a messy, inconsistent hybrid that creates opportunities for tax avoidance and distorts investment decisions—primarily due to the continued deductibility of interest payments.

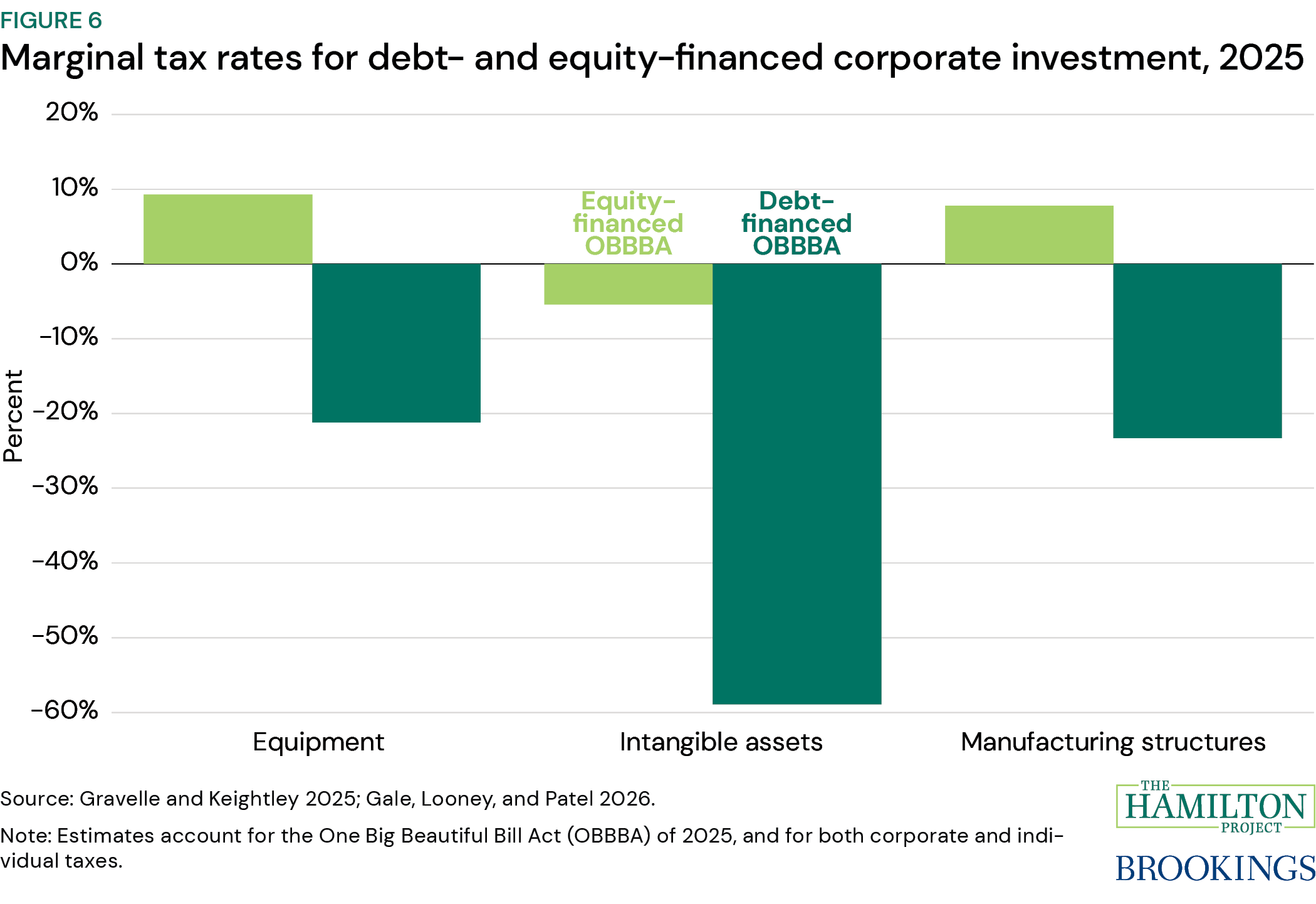

For equity-financed investments earning normal returns, the current corporate tax achieves a zero tax rate because the investment is deducted up front, and the returns are taxed. For debt-financed investments, however, the investment is deducted up front, and the returns are deducted in the form of interest payments. As shown in figure 6, the resulting tax rate is often highly negative (i.e., a firm makes more money from the investment because of the tax system) (Gravelle and Keightley 2025). (The tax rates shown in figure 6 include both business and individual taxes paid, which is why the tax rate on certain equity-financed corporate investments is positive rather than zero.) Negative tax rates invite the development of new tax shelters, distort businesses’ choices of how to finance investments, and can even lead to wasteful investments made just for tax reasons.

Gale, Looney, and Patel argue that the right response to these problems is to embrace the shift to a cash-flow tax and complete it, by eliminating interest deductibility and allowing expensing of additional categories of investment.9 This approach could raise on the order of $400 billion over 10 years (2027–36), the authors estimate, while allowing the U.S. to realize the economic benefits of a true business cash-flow tax. They also recommend reforming the domestic tax base by eliminating tax expenditures other than those linked to clear positive externalities (such as tax benefits for research and clean energy); implementing these recommendations could yield additional savings.

Clausing also endorses broadening the domestic corporate tax base by eliminating or curbing interest deductibility.

Taxation of large or complex pass-throughs. Johnson, Spinrad, Bryant, and Huang confront the challenges posed by the differential tax treatment of pass-through businesses and the growth of the pass-through sector. Their paper examines an approach that many policymakers have offered to address these problems: requiring large or complex pass-through entities to pay federal income tax at the entity level, like C corporations do. To evaluate this approach, they develop and analyze a concrete proposal to convert the tax treatment of pass-through entities with gross receipts averaging more than $25 million over a three-year period to C corporation tax treatment.

By imposing uniform tax treatment on the largest U.S. businesses, this proposal could reduce opportunities for these businesses to choose whichever tax laws result in the lowest tax bill, the electivity that has driven so much of the decline in business tax revenue over time. The proposal could also curtail the tax avoidance opportunities that large firms have exploited using partnership tax rules that were originally written with small, simple entities in mind (Johnson et al. 2024).

The Urban-Brookings Tax Policy Center estimates that the proposal, with the $25 million gross receipts threshold, would raise nearly $140 billion over 10 years (2027–36), with revenue growing to over $25 billion annually by 2035. The policy would result in C corporation tax treatment for about 0.7 percent of pass-through businesses and nearly half of pass-through income. While these estimates take into account that some businesses will try to avoid the tax (for example, by reorganizing themselves to game the gross receipts threshold), the true revenue gains could be smaller if avoidance is more widespread than anticipated. On the other hand, the estimates largely omit what could be substantial savings from addressing tax-sheltering opportunities created by gaps in current partnership tax rules and from improving IRS visibility into the operations and earnings of large and complex partnerships.

Johnson, Spinrad, Bryant, and Huang emphasize that implementation would not be easy, with especially challenging issues around properly measuring entity size and transitioning to the new system. Their proposal makes recommendations for how to address some of the thorny issues involved, such as which separately organized but jointly owned businesses should be treated as single entities. Despite the challenges, they conclude the proposal deserves consideration as a way to achieve a more rational business tax system with greater revenue-raising capacity, especially given obstacles to other pass-through tax reforms and particularly if adopted in conjunction with a corporate rate increase (as discussed further below).

As the authors discuss, policymakers could also consider going further toward a uniform system of business taxation by setting a lower gross receipts threshold. For example, a $10 million threshold would cover an estimated 63 percent of pass-through income, while still requiring only 1.3 percent of pass-through entities to transition to C corporation tax treatment.10

International tax. Both the Gale, Looney, and Patel and the Clausing proposals identify the U.S. tax system’s treatment of foreign earnings and foreign businesses as a major target for reform.

Clausing proposes to build on the multilateral “Pillar Two” reforms to the international tax system. The underlying principle of these reforms is that all business income worldwide should be taxed at a rate of at least 15 percent. This “global minimum tax” requirement reduces the role of tax havens and lessens incentives to shift income and profits for tax reasons; it also reduces the tax competition pressures that drive jurisdictions to lower corporate tax rates.

Clausing argues that the United States has a lot to gain from embracing the Pillar Two reforms—and a lot to lose if the multilateral framework falls apart due to U.S. opposition. A resurgence in race-to-the-bottom tax competition could have particularly large revenue costs for the United States. Conversely, with U.S. support, the Pillar Two framework would likely be even more stable, serving as a solid foundation for future efforts to strengthen and simplify international tax cooperation.

Clausing therefore proposes that the United States reform its current minimum tax on foreign earnings to meet Pillar Two standards, in particular by applying the minimum tax on a country-by-country basis. (This means applying the minimum tax separately to a businesses’ earnings from each foreign country, rather than allowing income from some countries to be taxed at less than the minimum rate if income from other countries is taxed at higher rates.)

She also argues that the United States would benefit from setting a minimum tax rate on foreign earnings well above the Pillar Two 15 percent standard, closer to the U.S. domestic rate. Specifically, she recommends a minimum tax on foreign earnings equal to 85 percent of the domestic corporate rate (about 18 percent under current law, or about 23 to 25 percent for major U.S. multinational companies under her proposal, which would also increase the domestic rate for large C corporations). Overall, Clausing’s proposed international reforms, if implemented independently, would raise in the range of $1 trillion over 10 years (2027–36), based on Penn Wharton Budget Model estimates.

Gale, Looney, and Patel instead propose to address international tax avoidance through a shift to a destination-based business tax system. Conceptually, the current U.S. tax system aims to tax the profits arising from both U.S. and foreign production of U.S. firms (albeit with reduced rates on foreign earnings and with tax credits for foreign taxes paid), as well as the profits of foreign firms operating in the United States. Under a destination-based tax, the United States would aim to tax the profits arising from U.S. sales. This would be implemented through a border adjustment tax levied on imports and rebated on exports; the authors estimate that the border adjustment would raise about $2.6 trillion over 10 years at the current 21 percent corporate rate.

A major advantage of a destination-based tax is that it likely leaves less scope for avoidance than the current source-based system, because it is generally harder to change or disguise the location of sales than production (although this may be less true for digital sales). But as both Gale, Looney, and Patel and Clausing discuss, there are significant challenges to a unilateral U.S. shift to a destination-based tax. First, it would likely destabilize the Pillar Two framework, which risks reigniting a global race-to-the-bottom in corporate tax rates. Second, it could be seen as another significant bad faith action by the United States, with potential consequences for global relations beyond tax policy. Third, adopting a border adjustment on a unilateral basis could lead the dollar to appreciate. Because foreigners invest more in the United States than U.S. residents invest abroad, this would result in a large wealth transfer to foreign investors. Finally, unilateral U.S. adoption of a border-adjusted tax would likely be challenged as violating World Trade Organization requirements. These problems would be mitigated or avoided under a negotiated, multilateral shift to destination-based taxes.

Increasing the corporate rate. Adopting the proposals above—especially in combination—would increase the revenue from, and reduce economic distortions from, increasing the corporate tax rate (see table 1). Completing the shift to a cash-flow tax means that increases in the corporate tax rate generally should not reduce the total amount of business investment, and, with interest no longer deductible, they also should not distort businesses’ choice of financing. While the corporate tax rate could still influence businesses’ decisions about whether to invest in the United States or abroad, as well as whether to use tax avoidance strategies to shift profits outside of the United States, these incentives would be significantly mitigated under Clausing’s proposal for a stronger U.S. minimum tax on foreign earnings and by the Pillar Two framework, which would be strengthened by U.S. participation. Further, corporate rate increases are typically expected to lead to a shift toward the use of pass-through entities, shrinking the corporate base, but this incentive would be sharply reduced if all large businesses were required to pay tax as C corporations.

What might be an appropriate tax rate for a reformed corporate tax? All three proposals discussed above advocate for increasing the corporate rate from the current 21 percent. Gale, Looney, and Patel propose a 25 percent rate, in part to keep the border adjustment (the tax on imports and rebate on exports) at workable levels; they also note that a cash-flow tax could allow for a higher corporate rate with minimal economic distortions. Johnson, Spinrad, Bryant, and Huang emphasize that taxing large or complex pass-throughs as corporations and increasing the corporate rate are strongly complementary revenue raisers and present illustrative estimates for 22 and 30 percent corporate rates. Clausing advocates for a graduated rate structure with a rate of 29.7 percent for the largest corporations that comprise about 90 percent of the corporate tax base.

Other reference points come from prior presidential and congressional proposals. In 2012, former President Barack Obama proposed to reform the corporate tax and lower the rate from 35 to 28 percent, a level the administration argued would be in line with other large developed countries (White House and U.S. Department of the Treasury 2012). In 2014, then-Ways and Means Committee Chair Dave Camp proposed a reform with a 25 percent rate, which at the time was also the recommendation of the Business Roundtable (U.S. House Committee on Ways and Means 2014; Becker and Bogardus 2013). In 2017, President Donald Trump pressed for a reduction in the corporate rate from 35 to 20 percent, ultimately securing a 21 percent rate as part of the Tax Cuts and Jobs Act (TCJA) of 2017. Since then, prominent proposals to raise revenue by reversing the TCJA corporate rate cut have generally proposed rates no higher than the 28 percent rate proposed by former President Obama. In particular, former President Biden’s budgets proposed a 28 percent rate, and the Ways and Means Committee version of the 2021 Build Back Better Act included a 26.5 percent rate.

A 28 percent rate has remained focal for policymakers even as conditions have changed in ways that suggest higher rates might be appropriate.

First, the fiscal situation has deteriorated. The actual fiscal year 2025 deficit was 5.8 percent of GDP, versus CBO projections of 3.7 percent as of 2012 (when former President Obama proposed a 28 percent corporate rate), 4.2 percent as of 2014 (when then-Chairman Camp proposed 25 percent), and 4.0 percent as of 2021 (when former President Biden proposed 28 percent) (Congressional Budget Office 2011, 2014, 2021). Interest rates on federal debt are also higher today than when any of those proposals were released. All else equal, higher deficits and higher interest rates increase the value of additional revenue.

Second, the international context has changed. Proposals to lower the corporate rate in the 2010s were motivated in large part by competitiveness concerns, with advocates of both a 28 percent and a 25 percent rate arguing these rates would put the U.S. rate in line with those of peer countries. But these proposals predated the Pillar Two agreement. Pillar Two implementation is already reducing pressure on the U.S. international tax system from very low-rate tax havens. Additionally, since the agreement was adopted in 2021, the GDP-weighted worldwide average corporate rate and the G7 average, excluding the U.S., have ticked up slightly, following years of declines (Enache 2025). All else equal, reduced international tax competition argues for a higher U.S. corporate tax rate.

Third, even without additional reforms, the OBBBA of 2025 has already moved the U.S. corporate tax much of the way toward a cash-flow tax, with expensing for most investment. In contrast, the Biden administration budgets and Ways and Means Committee Build Back Better Act proposals assumed continued depreciation for most investment. All else equal, expensing reduces the economic cost of a corporate rate increase.

Given these changes, corporate tax rates above 28 percent warrant consideration, especially in the context of the additional reforms discussed above.

As an illustrative example, the Tax Policy Center estimates that increasing the corporate rate to 30 percent would raise $1.2 trillion over 10 years (2027–36), or $138 billion annually by 2035. If enacted on top of the higher corporate rate, the proposal to tax pass-throughs with over $25 million in gross receipts as C corporations would raise $468 billion over 10 years, or $63 billion annually by 2035. Clausing’s proposed international reforms would raise an additional $1.4 trillion (2027–36), or about $160 billion annually by 2035, if implemented after an increase in the corporate rate, based on estimates from the Penn Wharton Budget Model.11 Gale, Looney, and Patel estimate that completing the shift to a cash-flow tax would add about $400 billion (2027–36), or in the range of $45 billion annually by 2035.

Thus, a combined reform along these lines could raise well over $3 trillion over 10 years or more than $400 billion (0.9 percent of GDP) annually by 2035—in historical terms, roughly equivalent to reversing the decline in the corporate tax since the late 1990s.12 Such a reform—or other, similar approaches to raising additional revenue from business taxes—would represent a meaningful step toward a progressive tax system that can raise the revenue to meet current national needs.

Acknowledgments

I would like to thank Tia Cole and Eileen Powell for excellent research assistance and Lily Batchelder, Lauren Bauer, Kathleen Bryant, Kimberly Clausing, Brendan Duke, William Gale, Chye-Ching Huang, Samantha Jacoby, Miles Johnson, David Kamin, Chuck Marr, Thalia Spinrad, and Danny Yagan for helpful comments.

Endnotes

[1] The figure shows calendar year corporate tax payments, which differ slightly from the fiscal year corporate revenues reported in the text.

[2] Following the approach used in Congressional Budget Office (2023), I approximate C corporation economic profits using National Income and Product Accounts data on the combined economic profits of C and S corporations and Internal Revenue Service data on the C corporation share of taxable profits. Using this approach, corporate tax payments as a share of C corporation economic profits fell from over 25 percent in the late 1970s to an average of about 13 percent in the years following the 2017 tax law (2018–22).

[3] Moreover, 2022 was an anomalous year, with corporate revenues driven up by the recovery from the pandemic. As of 2019, the total effective tax rate on the top 1 percent was 30 percent, and the effective corporate rate was 4.2 percent.

[4] The estimates of effective tax rates for the top 1 percent and the top 400 are not directly comparable. In particular, CBO’s estimates of effective tax rates for the top 1 percent do not include unrealized capital gains in income, while Balkir et al. (2025)’s estimates do include unrealized gains in income.

[5] Another approach to addressing the challenge of unrealized capital gains is taxation at death, as former President Biden (among others) proposed (U.S. Department of the Treasury 2021). While not as robust as annual taxation of unrealized gains, this policy does not raise the legal or administrative concerns discussed, and it would still reduce the tax benefits of deferral (and the incentive to convert other wealth into unrealized gains) by preventing assets bequeathed to heirs from avoiding tax altogether. It would be strongly complementary to other approaches to increasing taxes on capital income, whether through business or individual reforms.

[6] Indeed, for the portion of capital gains attributable to corporations’ retained earnings, entity-level business taxes offer a direct mechanism for taxing unrealized gains: Policymakers can achieve their desired level of tax on this income at the entity level. Corporate retained earnings account for a minority of capital gains income, and business entity taxes do not reach the majority of capital gains income attributable to appreciation of corporate stock and other assets unrelated to retained earnings (Campbell et al. 2025). However, unlike individual-level taxes, they don’t need to reach this income to effectively tax other capital income.

[7] Some proposals, including those from former President Biden and Sen. Wyden, address this issue by allowing taxpayers to defer tax on illiquid assets until they are sold and then pay the tax with interest. While this limits administrative burden, it can distort asset allocations if the deferral charge is too low or if taxpayers think there is a reasonable likelihood it will not be levied.

[8] A cash-flow tax can still create incentives to shift investments earning supernormal returns to lower-tax countries, an issue discussed below.

[9] Batchelder (2026) makes the case for instead correcting the problem by repealing expensing. She notes that the economic case for expensing depends on the assumption that businesses respond to the marginal rate on investment rather than the statutory or book tax rate, which may or may not hold in practice.

[10] The proposal also discusses other alternatives, including higher thresholds and triggers based on a business’ total assets or indicators of business complexity, rather than gross receipts.

[11] Clausing reports estimates for the 2030–39 period, when the international reforms raise an estimated $1.6 trillion if enacted independently.

[12] These estimates are approximate, especially because they combine estimates from different modelers, but they are conservative in that they do not account for the interaction between the broader domestic tax base and the 30 percent rate or pass-through reforms, and the international estimates assume Clausing’s graduated rates, not a 30 percent rate.

References

Balkir, Akan S., Emmanuel Saez, Danny Yagan, and Gabriel Zucman. 2025. “How Much Do Billionaires Pay? Evidence From Administration Data.” Working Paper 34170, National Bureau of Economic Research, Cambridge, MA. https://www.nber.org/papers/w34170.

Batchelder, Lily L., and David Kamin. 2019. “Policy Options for Taxing the Rich.” In Maintaining the Strength of American Capitalism. The Aspen Institute, Washington, DC. https://www.economicstrategygroup.org/publication/policy-options-for-taxing-the-rich/

Batchelder, Lily L. 2026. “When Money’s Time Isn’t Always Valued: Accounting for Behavioral Considerations in Business Tax Reforms.” Working paper 6921418. Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6921418.

Becker, Bernie, and Kevin Bogardus. 2013. “CEOs set tax reform goal: 25 percent corporate rate.” The Hill, March 18. https://thehill.com/policy/finance/145123-ceos-set-tax-reform-goal-25-percent-corporate-rate/

U.S. Bureau of Economic Analysis. 2026a. “Table 1.1.5 Gross Domestic Product. “Accessed April 16, 2026. https://apps.bea.gov/iTable/?reqid=19&step=2&isuri=1&categories=survey

U.S. Bureau of Economic Analysis. 2026b. “Table 1.12. National Income by Type of Income.” Accessed April 16, 2026. https://apps.bea.gov/iTable/?reqid=19&step=2&isuri=1&categories=survey

U.S. Bureau of Economic Analysis. 2026c. “Table 3.2 Federal Government Current Receipts and Expenditures.” Accessed April 16, 2026. https://apps.bea.gov/iTable/?reqid=19&step=2&isuri=1&categories=survey

Campbell, Cole, Jacob A. Robbins, and Sam Wylde. 2025. “The distribution of capital gains in the United States.” The Washington Center for Equitable Growth, Washington, DC. https://equitablegrowth.org/working-papers/the-distribution-of-capital-gains-in-the-united-states/

Clausing, Kimberly. 2020. “How Big Is Profit Shifting?” Working Paper 3503091. Available at SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3503091

Clausing, Kimberly. 2026. “The Future of US International Corporate Tax Reform.” The Hamilton Project, Brookings Institution, Washington, DC. https://www.hamiltonproject.org/publication/policy-proposal/the-future-of-us-international-corporate-tax-reform/

Committee for a Responsible Federal Budget. 2025. “What’s in the One Big Beautiful Bill Act.” Committee for Responsible Federal Budget, Washington, DC. https://www.crfb.org/blogs/whats-one-big-beautiful-bill-act

Congressional Budget Office (CBO). 2011. CBO’s 2011 Long-Term Budget Outlook. Congressional Budget Office, Washington, DC. https://www.cbo.gov/publication/41486

Congressional Budget Office (CBO). 2012. Taxing Businesses Through The Individual Income Tax. Congressional Budget Office, Washington, DC. https://www.cbo.gov/publication/43750

Congressional Budget Office (CBO). 2014. The 2014 Long-Term Budget Outlook. Congressional Budget Office, Washington, DC. https://www.cbo.gov/publication/45471

Congressional Budget Office (CBO). 2021. The Budget and Economic Outlook: 2021 to 2031. Congressional Budget Office, Washington, DC. https://www.cbo.gov/publication/56991

Congressional Budget Office (CBO). 2023. Trends in Corporate Economic Profits and Tax Payments, 1998 to 2017. Congressional Budget Office, Washington, DC. https://www.cbo.gov/publication/58267

Congressional Budget Office (CBO). 2026a. The Budget and Economic Outlook: 2026 to 2036. CBO, Washington, DC. https://www.cbo.gov/publication/62105

Congressional Budget Office (CBO). 2026b. The Distribution of Household Income, 2022. CBO, Washington, DC. https://www.cbo.gov/publication/61911

Cooper, Michael, John McClelland, James Pearce, et al. 2016. “Business in the United States: Who Owns It, and How Much Tax Do They Pay?” Tax Policy and the Economy 30 (1): 91–128. https://www.journals.uchicago.edu/doi/10.1086/685594

Enache, Christina. 2025. “Corporate Tax Rates Around the World, 2025.” Tax Foundation, Washington, DC. https://taxfoundation.org/data/all/global/corporate-tax-rates-by-country-2025/

Gale, William, Adam Looney, and Elena Patel. 2026. “Corporate Tax Reform in the Wake of the 2025 Tax Law: Completing the Shift to a Corporate Cash-Flow Tax.” The Hamilton Project, Brookings Institution, Washington DC. https://www.hamiltonproject.org/publication/policy-proposal/corporate-tax-reform-in-the-wake-of-the-2025-tax-law-completing-the-shift-to-a-corporate-cash-flow-tax/

Goodman, Lucas, Quinton White, and Andrew Whitten. 2024. “Taxing S Corporations as C Corporations.” Working Paper 126, U.S. Department of the Treasury, Washington, DC. https://home.treasury.gov/system/files/131/WP-126.pdf

Gravelle, Jane G. 2006. Historical Effective Marginal Tax Rates on Capital Income. Report RS21706. Congressional Research Service. https://www.congress.gov/crs_external_products/RS/PDF/RS21706/RS21706.6.pdf

Gravelle, Jane G., and Mark P. Keightley. 2025. Marginal Effective Tax Rates: Changes in P.L. 119-21, the 2025 Reconciliation Act. Report R48631, Congressional Research Service. https://www.congress.gov/crs-product/R48631

U.S. House Committee on Ways and Means. 2014. “Camp Formally Introduces the Tax Reform Act of 2014.” Press release, February 26. https://waysandmeans.house.gov/2014/12/11/camp-formally-introduces-the-tax-reform-act-of-2014/

International Revenue Service (IRS). n.d. “SOI Tax Stats – Integrated Business Data.” IRS, U.S. Department of the Treasury, Washington, DC.

International Revenue Service (IRS). n.d. “SOI Tax Stats – Corporation Income Tax Returns Complete Report (Publication 16).” IRS, U.S. Department of the Treasury, Washington, DC.

International Revenue Service (IRS). n.d. “Partnership Returns.” IRS, U.S. Department of the Treasury, Washington, DC.

International Revenue Service (IRS). n.d. “Sole Proprietorship Returns.” IRS, U.S. Department of the Treasury, Washington, DC.

Johnson, Miles, Thalia T. Spinrad, Kathleen Bryant, and Chye-Ching Huang. 2026. “Toward a Uniform Business Tax System: Examining Proposals to Tax Large Pass-Through Entities as Corporations.” The Hamilton Project, Brookings Institution, Washington DC. https://www.hamiltonproject.org/publication/policy-proposal/toward-a-uniform-business-tax-system-examining-proposals-to-tax-large-pass-through-entities-as-corporations/

Johnson, Miles, Sophia Yan, Chye-Ching Huang, and Grace Henley. 2024. “Modernizing partnership taxation.” The Hamilton Project, Brookings Institution, Washington DC. https://www.hamiltonproject.org/publication/policy-proposal/modernizing-partnership-taxation/

Joint Committee on Taxation. 2017. Estimated Budget Effects of the Conference Agreement for H.R.1, The Tax Cuts and Jobs Act. Joint Committee on Taxation, Washington, DC. https://www.jct.gov/publications/2017/jcx-67-17/

Liscow, Zachary. 2026. “The Simple Answer to Taxing the Rich Is the Best Answer.” The New York Times, May 22. https://www.nytimes.com/2026/05/22/opinion/wealth-tax-millionaires-policy.html

Office of Sen. Bernie Sanders. 2026. “NEWS: Sanders and Khanna Introduce Legislation to Tax Billionaire Wealth and Invest in Working Families.” Press release, March 2. https://www.sanders.senate.gov/press-releases/news-sanders-and-khanna-introduce-legislation-to-tax-billionaire-wealth-and-invest-in-working-families/

Office of Sen. Elizabeth Warren. 2026. “Warren, Jayapal, Boyle, 45+ Lawmakers Renew Push for Wealth Tax on Ultra-Millionaires and Billionaires.” Press release, March 26. https://www.warren.senate.gov/newsroom/press-releases/warren-jayapal-boyle-45-lawmakers-renew-push-for-wealth-tax-on-ultra-millionaires-and-billionaires

Pomerleau, Kyle. 2024. Addressing Business Tax “Parity” Through Integration. AEI Economic Perspectives. American Enterprise Institute, Washington, DC. https://www.aei.org/research-products/report/addressing-business-tax-parity-through-integration/

U.S. Senate Committee on Finance. 2025. “Wyden, Cohen, Beyer Introduce the Billionaires Income Tax Act.” Press release, September 17, 2025. https://www.finance.senate.gov/ranking-members-news/wyden-cohen-beyer-introduce-the-billionaires-income-tax-act

Smith, Matthew, Danny Yagan, Owen Zidar, and Eric Zwick. 2019. “Capitalist in the Twenty-First Century.” The Quarterly Journal of Economics 134 (4): 1675–745. https://academic.oup.com/qje/article-abstract/134/4/1675/5542244

Smith, Matthew, Owen Zidar, and Eric Zwick. 2023. “Top Wealth in America: New Estimates Under Heterogeneous Returns.” The Quarterly Journal of Economics 138 (1): 515–73. https://academic.oup.com/qje/article/138/1/515/6678447

U.S. Department of the Treasury. 2022. General Explanations of the Administrations Fiscal Year 2022 Revenue Proposals. U.S. Department of the Treasury, Washington, DC. https://home.treasury.gov/system/files/131/General-Explanations-FY2022.pdf

U.S. Department of the Treasury. 2024. General Explanations of the Administrations Fiscal Year 2025 Revenue Proposals. U.S. Department of the Treasury, Washington, DC. https://home.treasury.gov/system/files/131/General-Explanations-FY2025.pdf

Rosenthal, Steven M., and Livia Mucciolo. 2024. “Who’s Left to Tax? Grappling With a Dwindling Shareholder Tax Base.” Tax Notes, April 1. https://www.taxnotes.com/featured-analysis/whos-left-tax-grappling-dwindling-shareholder-tax-base/2024/03/29/7j9cr

The White House and the U.S. Department of the Treasury. 2012. The President’s Framework for Business Tax Reform. White House and the U.S. Department of the Treasury, Washington DC. https://home.treasury.gov/system/files/131/OTA-Report-Business-Tax-Reform-2012.pdf

Wright, Thomas, and Gabriel Zucman. 2018. “The Exorbitant Tax Privilege.” Online appendix to working paper. HM Treasury and UC Berkeley. https://gabriel-zucman.eu/files/WrightZucman2018Appendix.pdf.