The challenge

U.S. business taxes are an essential part of taxing U.S. capital income; much U.S. capital income goes untaxed at the individual level, and what is taxed is taxed very lightly in comparison with labor income. At the same time, U.S. corporate tax revenues are very low compared to peer nations, even as U.S. fiscal challenges have become more acute. U.S. deficit and debt levels are projected to become particularly alarming in the coming decade.

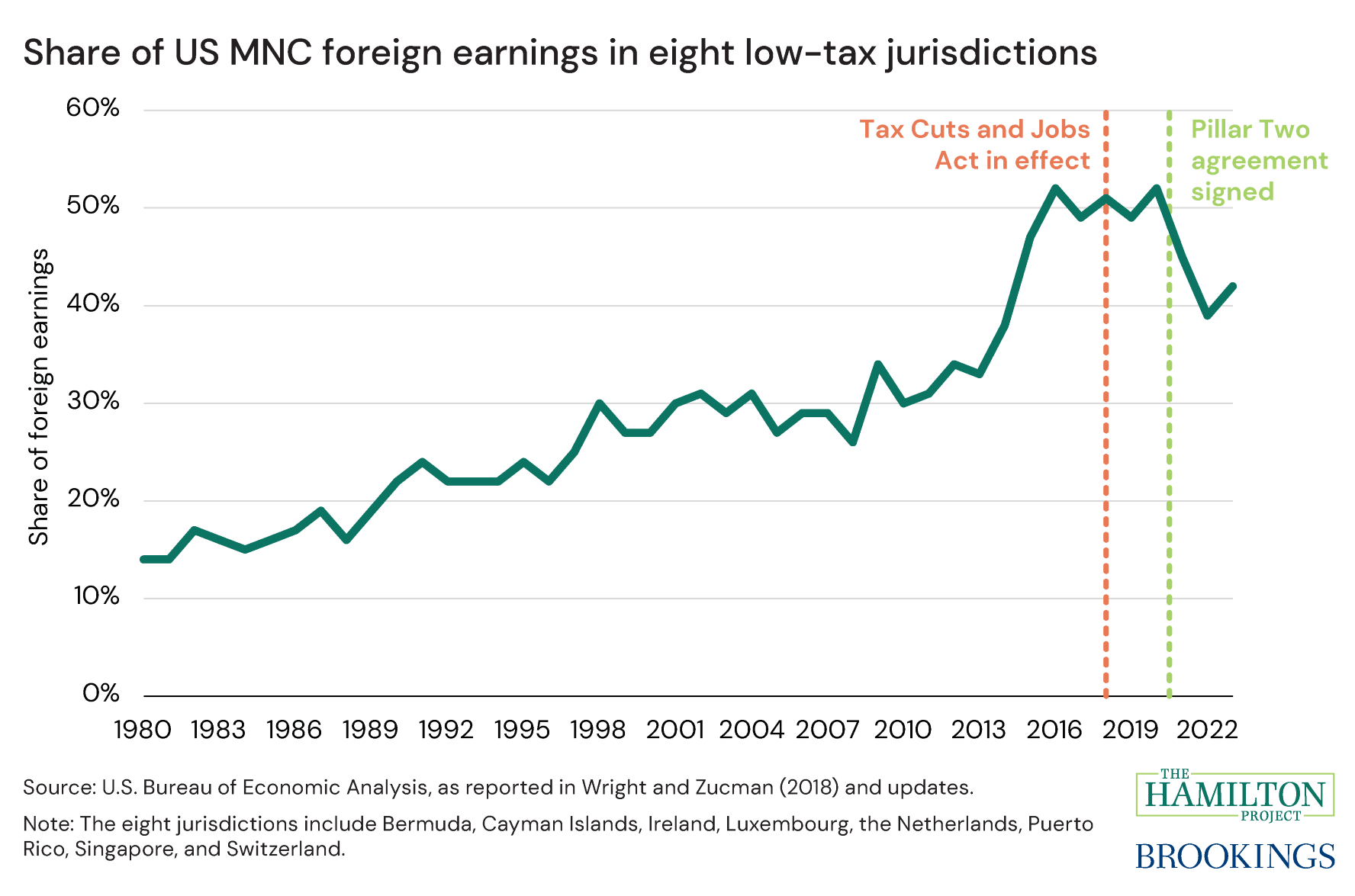

There are multiple reasons for low U.S. corporate revenues, including recent changes to U.S. corporate tax law as well as a large share of pass-through business activity in the United States. Still, international profit shifting continues to be an important driver of the erosion of the U.S. corporate tax base. The U.S. international corporate tax system has long featured, and continues to feature, a large distortion in favor of foreign income relative to U.S. income. U.S. multinational corporations book vastly disproportionate earnings in the lowest-tax rate jurisdictions, suggesting substantial tax-motivated profit shifting.

International tax avoidance creates a global collective action problem. Governments that would like to strengthen their taxation of multinational corporate income are deterred by the mobility of multinational corporate income and concerns about preserving competitiveness relative to other countries.

In 2021, countries around the world, including the United States, took a major step toward addressing this collective action problem, uniting around the “Pillar Two” framework for a global 15 percent minimum tax on multinational corporate income. After the European Union moved forward unanimously in late 2022 to implement Pillar Two, implementation occurred in many more countries during 2023 and 2024. However, in 2025, the Trump administration rejected the international tax agreement, ultimately resulting in a “side-by-side” arrangement that effectively exempts U.S. multinational firms from key provisions of the global tax deal. This side-by-side regime has weakened the agreement and expanded both tax competition pressures and corporate tax base erosion possibilities.

The proposal

Kimberly Clausing (UCLA Law) proposes to strengthen and reform U.S. corporate taxation while better aligning U.S. corporate tax policy efforts with the large potential of international collective action.

The key features of the proposal are the following:

Corporate tax rate and base. The corporate tax rate would be raised to 27 percent for corporations with more than $5 million in income; an additional surtax of 10 percent of tax liability, resulting in an effective rate of 29.7 percent, would apply to corporations with more than $50 million in income. These tax rate increases would apply to fewer than 2 percent of corporate taxpayers, but they would include more than 95 percent of the corporate tax base. The higher rate would be accompanied by a broader corporate tax base that moves the corporate tax base closer to a tax on pure profits.

Minimum tax on foreign income. The U.S. would institute a reformed minimum tax on the foreign income of U.S. multinational firms with a 15 percent deduction relative to the domestic rate, resulting in rates of approximately 23 or 25 percent on nearly all foreign income. The U.S. would also adopt the backstop provision of the Pillar Two tax framework, the under-taxed profits rule (UTPR). The U.S. export subsidy policy (FDDEI, formerly FDII) would be repealed. Other U.S. minimum taxes (BEAT and CAMT) would be “turned off” for many taxpayers, as they would no longer be necessary.

Improvements to Pillar Two. After enacting these reforms, the U.S. would partner with other governments in another round of international negotiations on international tax, with the aim of strengthening and simplifying international collective action around tax competition. Clausing argues that the U.S. has a lot to gain from embracing the Pillar Two reforms—and a lot to lose if the multilateral framework ultimately falls apart due to U.S. opposition. With U.S. support, the Pillar Two framework would likely be even more stable, serving as a solid foundation for future efforts to strengthen and simplify international tax cooperation.

This proposal would raise about 0.9 percent of GDP in new tax revenue, $4.0 trillion in revenue over the 2030–39 budget window (or $3.4 trillion from 2026-35), the Penn Wharton Budget Model estimates. The policies would also make the tax system more progressive, more administrable, and would better align the U.S. corporate tax system with efforts to tackle tax competition and profit shifting abroad, setting the stage for more productive cooperative efforts on economic governance.