The challenge

The U.S. tax system raises insufficient revenue to meet national needs. One contributor to the shortfall is the erosion of taxes on business income, due in part to increases in the use, scale, and complexity of pass-through entities.

Businesses are generally taxed either as corporations under subchapter C (C corporations) or as some type of pass-through entity. C corporations face an entity-level federal income tax at a rate of 21 percent, with additional taxes on dividends and capital gains that flow to their owners. Pass-through entities, such as partnerships, S corporations, and sole proprietorships, generally do not pay federal income tax at the entity level; instead, their income, or loss, “passes through” to their owners, who pay any associated taxes.

Businesses have substantial flexibility to choose whether to organize as C corporations or pass-throughs, and the decision is often made based on taxes. On average, pass-through income is subject to less tax than the income of C corporations. That’s partly because of statutory rate differentials and the fact that pass-throughs face only one layer of tax and partly because S corporations and partnerships can often take advantage of loopholes, flexibilities, and planning opportunities not available to C corporations. Additionally, as pass-through entities have increased in number and complexity, pass-through tax rules have become more and more difficult to apply, administer, and enforce. The complexity of partnerships in particular has stymied IRS tax enforcement. As of 2019, the IRS audit rate for large partnerships had dropped below 0.5 percent, compared to a 5 percent audit rate for large corporations.

Lower tax rates, additional avoidance opportunities, and weak tax enforcement for large pass-through businesses cost the federal government significant revenue. These tax disparities can also distort businesses’ choice of structure and financing, encourage wasteful tax planning, and advantage industries and occupations that can organize as pass-throughs more easily than others.

The proposal

Miles Johnson, Thalia T. Spinrad, Kathleen Bryant, and Chye-Ching Huang (The Tax Law Center at NYU Law) examine an approach that many policymakers have offered to address these problems: requiring large or complex pass-through entities to pay federal income tax at the entity level, as corporations do. The charge to tax large or complex pass-throughs like corporations is not simple in practice, however, and existing proposals have generally been light on details.

To fill that gap, the authors develop and analyze a concrete proposal to require partnerships and S corporations with gross receipts over $25 million to be taxed as C corporations. The authors discuss and offer solutions to design, transition, and implementation challenges, including how to measure gross receipts, which types of pass-through entities to include, and when to treat different business entities with significant common ownership as part of a single large business. The authors also analyze certain variations and alternatives that warrant further consideration, such as proposals that would impose corporate treatment based on characteristics other than size.

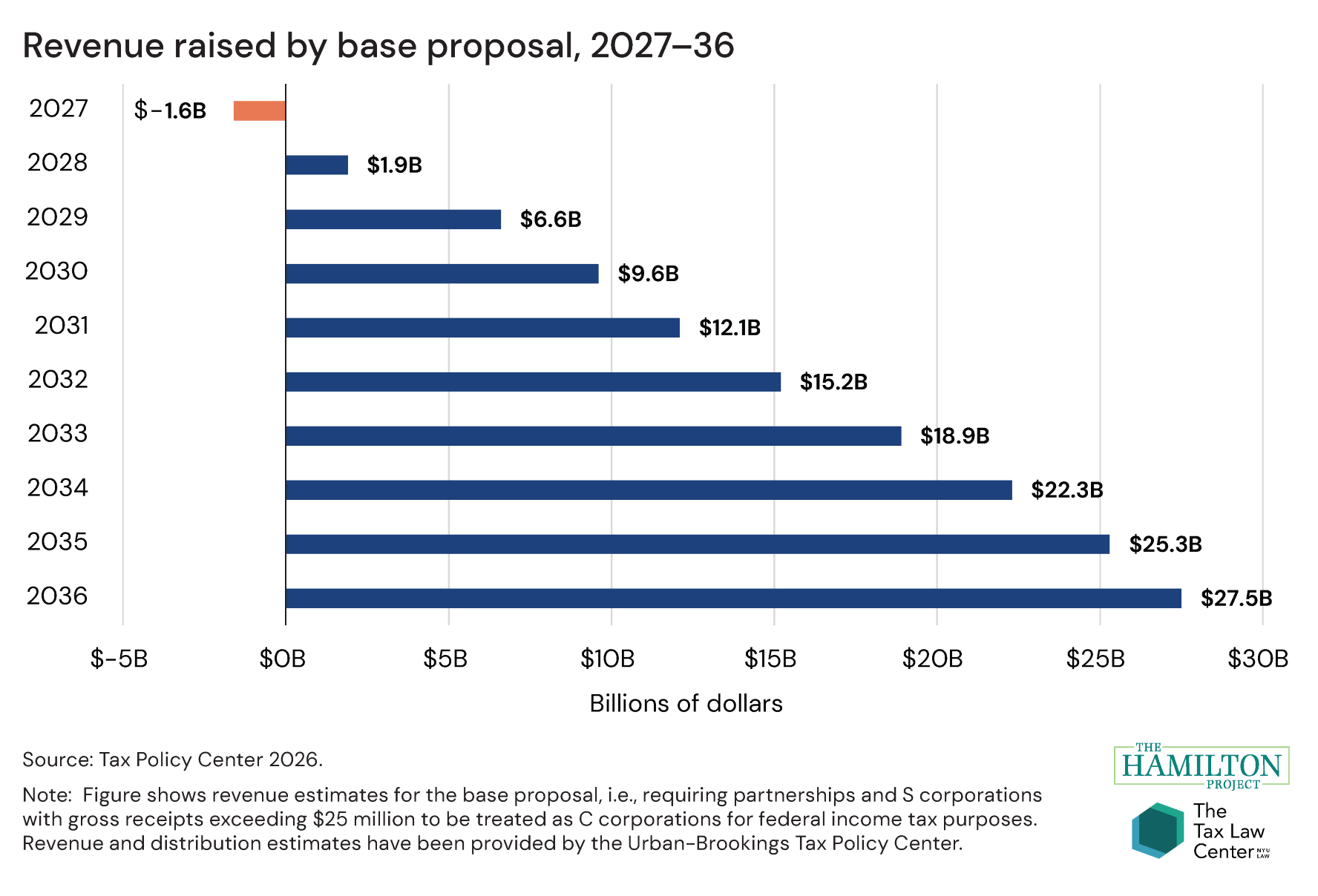

The proposal they analyze would raise nearly $140 billion over 10 years and over $25 billion annually by 2035, the Urban-Brookings Tax Policy Center estimates. This would increase to nearly $470 billion over 10 years and more than $63 billion annually by 2035 if the proposal were enacted after raising the corporate tax rate to 30 percent (revenue gains over and above what the corporate rate increase would raise on its own). The proposal would affect only the largest 0.7 percent of pass-throughs while reaching nearly half of pass-through income. Nearly 95 percent of additional taxes would be paid by the highest-income (top 10 percent) Americans, and about two thirds by the top 1 percent; further, by construction, the proposal would generally exclude small businesses. And while it presents significant transition and implementation challenges, the proposal could also provide benefits for tax administration by moving entities out of administratively challenging pass-through tax regimes.

Overall, the proposal has the potential to raise substantial revenue, reduce tax distortions, and simplify and improve tax administration and enforcement over the long run. However, it is also complex and likely to be unworkable without careful and detailed policy design. Given the need for additional revenue, the increasing challenges with current pass-through taxation, and potential obstacles to other pass-through tax reforms, the authors conclude that the proposal belongs on the menu for business tax reform, especially if adopted in conjunction with an increase in the corporate rate.